Should the recent GDP slump affect the 2013 federal budget?

The short answer is no. So is the long answer. Here’s why.

Finance Minister Jim Flaherty has gone public in a deeply personal interview with The Globe and Mail to explain some recent changes to his appearance. To quell concerns that his face has grown bloated and puffy and heâs gained a significant amount of weight, Flaherty gave the interview, explaining that he has a rare skin disease, called bullous pemphigoid, that requires strong steroid treatment. Flaherty is shown responding to a question during question period in the House of Commons Monday January 28, 2013 in Ottawa. THE CANADIAN PRESS/Adrian Wyld

Share

The short answer is: apart from forcing government forecasters to update their near-term projections, it shouldn’t.

One longer answer starts with the national accounts identity:

GDP = Consumption + Investment + Government + Net exports

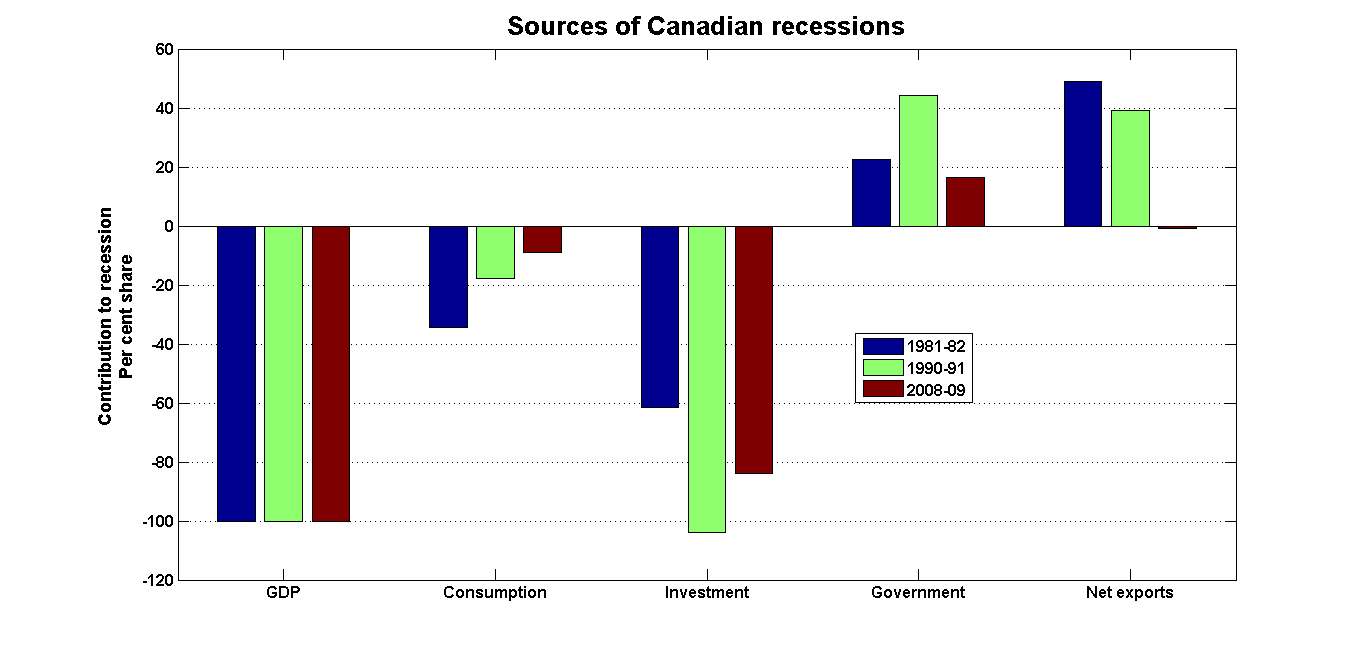

Changes in GDP can be attributed to changes in these expenditure categories. The charts below break down the contributions to the GDP growth during the past few business cycles. Both charts show the per cent contributions to the total increase or decrease in GDP. Here’s what happened during recessionary periods:

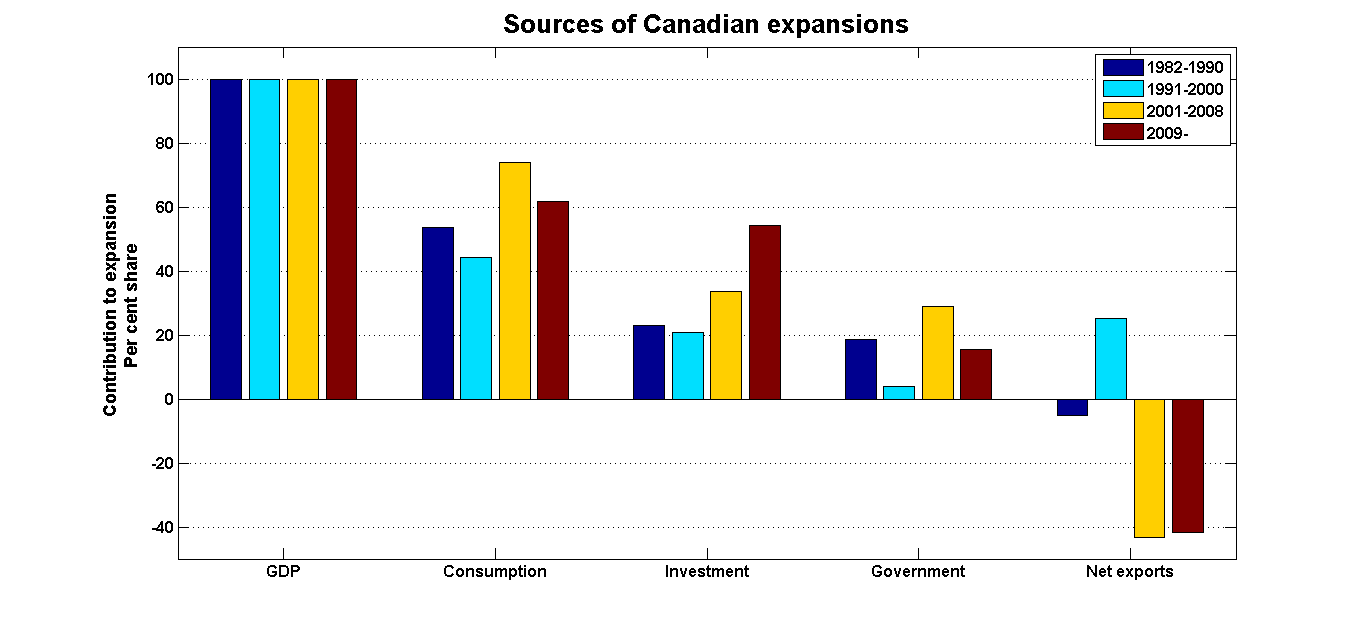

And here’s what expansionary periods look like:

There are a couple of things to take away from these graphs. This first is the importance of investment spending in driving the business cycle. The second is the fact that net exports are generally counter-cyclical: making a positive contribution during recessions, and (usually) acting as a drag on growth during expansions. This really shouldn’t be a surprise, but since trade deficits are invariably portrayed as bad news in the business press, it probably is a surprise.

Attentive Econowatch readers, though, will remember that the obverse side of a trade deficit (or, more precisely, a current account deficit) is an inflow of capital. To the extent that these capital inflows help finance an expansion based on increased investment, there’s little reason at all to portray trade deficits as bad news. Indeed, since recessions are invariably accompanied by a sharp depreciation of the Canadian dollar, the only time the trade balance makes consistently positive contributions to GDP growth is during recessions.

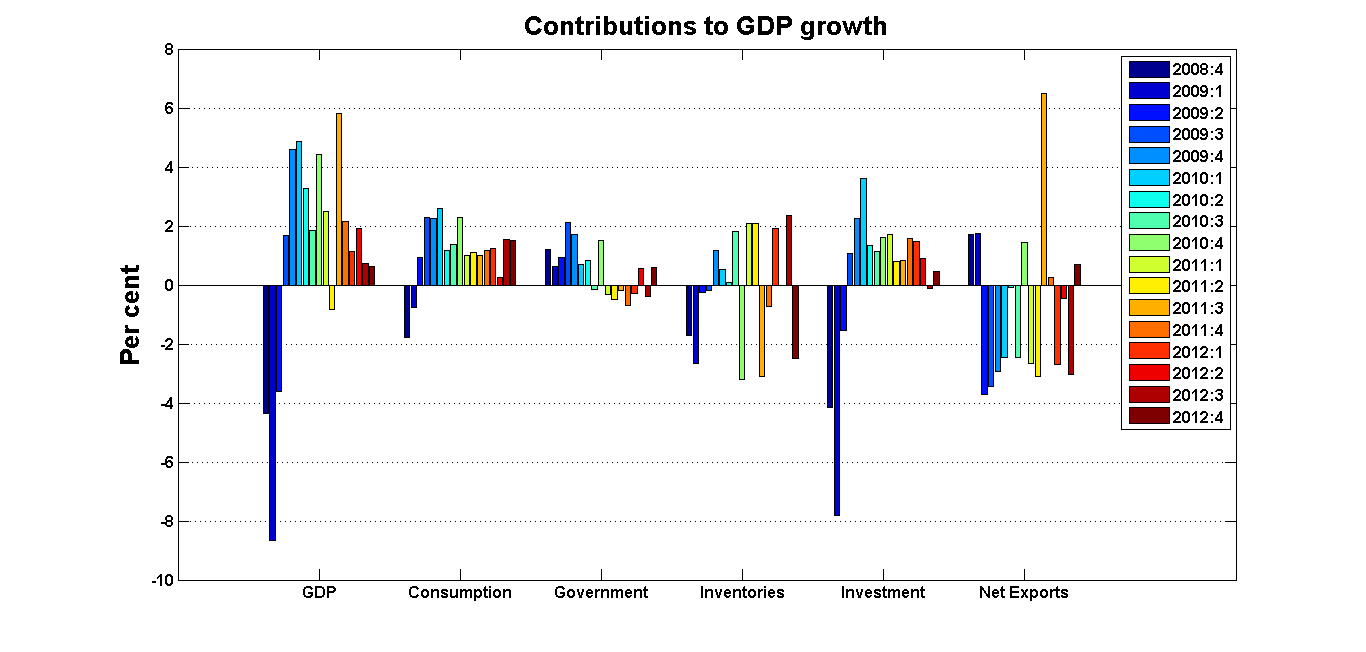

Let’s zoom in to the recent past. The next chart presents the contributions to GDP for each quarter since the beginning of the last recession. The height of the bars representing the change in GDP is the sum of the bar associated with each of its components:

Note that this chart separates changes in inventories from investment spending. (For a quick explanation of what inventory investment is and how it plays out in the business cycle, see here.) The national accounts classify changes in inventory holdings as part of investment, but it’s a good idea to break inventories out when looking at short-term fluctuations. Even though inventory holdings are relatively small, they are highly volatile and are a significant contributor to short-term movements in GDP. The most recent GDP release is a case in point: the drag induced by the drop in inventories subtracted more than two percentage points from the annualized fourth quarter GDP growth rate. If inventory holdings had stayed the same, the annualized growth rate in the last three months of 2012 would have been 3.1 per cent instead of 0.6 per cent. And if you take out the surge in inventories of the third quarter of 2012, the growth rate would have been -1.6 per cent instead of 0.7 per cent. When you look over the whole recovery/expansion period, the swings in inventories more or less cancel out, and you can see from the second chart that up until recently, investment growth has played a larger-than-usual role in driving GDP growth.

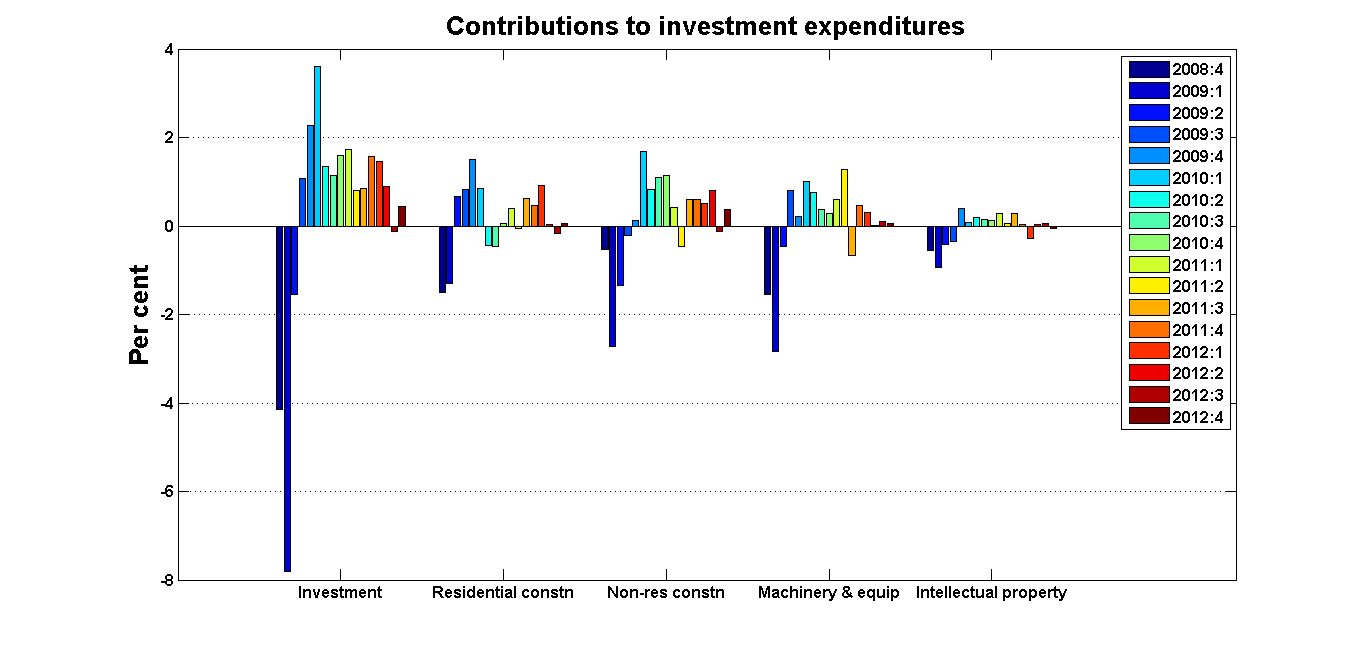

There are a couple more things you can see in the chart above. One is that net exports have been — again — a drag on growth in this expansion. Another is that governments pretty much stopped contributing to the recovery/expansion around the end of 2010. So it really is up to investment to sustain the expansion. Let’s zoom in again and look at investment broken down into its components:

The Bank of Canada has frequently referred to the investment “hand-off” or “pivot.” The first part of the recovery was driven by residential construction, but unless we’re willing to run the risk of a U.S.-style housing meltdown (and we’re not) there is a point at which pretty much everyone who is in a position to carry significant housing debt will have done so, and we’re near that point already — if we haven’t gone past it. So if investment is to continue to drive the expansion, it will have to be business investment: nonresidential construction and/or expenditures on machinery and equipment.

Now, business investment in the last six month of 2012 has disappointed. What should Finance Minister Flaherty do about it? Nothing, and here’s why:

- We’re not in a recession. Look at those charts: what we’re seeing now doesn’t look anything like a recession. Periods of sluggish growth in the midst of an expansion are common.

- Even if we were in a recession, fiscal policy is the clumsiest instrument in the policy arsenal and the most likely to see its effectiveness blunted by partisan political considerations. The much-vaunted stimulus program of the last recession didn’t really get underway until after the recession was over, and much of the spending was allocated to areas that didn’t actually need it. For example, even though the Quebec City area was largely spared from the ravages of the recession, my own riding — which happened to be represented by a cabinet minister — was showered with so many infrastructure projects that navigating the detours around construction projects became a daily challenge.

The Bank of Canada is better-placed to deal with business cycle policy than the Department of Finance. And although Flaherty has hinted at the possibility of spending cuts to offset lower-than-expected revenues, it’s far from clear that these measures are necessary: the deficit looks like it will come in below target for 2012-13. The recent data will change the next budget’s projections, but it shouldn’t affect the government’s policy stance.