Business investment hasn’t been this crummy in 40 years

Canadian companies remain nervous about the future, meaning the decline in business investment is unlikely to improve any time soon.

Bank of Canada Governor Stephen Poloz speaks about the Financial System Review during a news conference in Ottawa, Thursday,June 9, 2016. (Adrian Wyld/CP)

Share

When the Bank of Canada released its latest survey of business managers on Monday, it confirmed what we’ve known for some time now: companies in Canada are a panicked bunch. The Business Outlook Survey, conducted each quarter, found that business leaders view the next year with apprehension, particularly those with ties to the energy sector.

“Modest domestic demand, uncertainty and insufficient foreign demand are key factors holding back investment intentions,” the Bank observed, while noting the cautious outlook wasn’t limited to the oil patch. “While firms judge that the boost to their sales from U.S. growth is lending support to their investment plans, investment intentions are modest for exporters, even those unaffected by commodity prices.

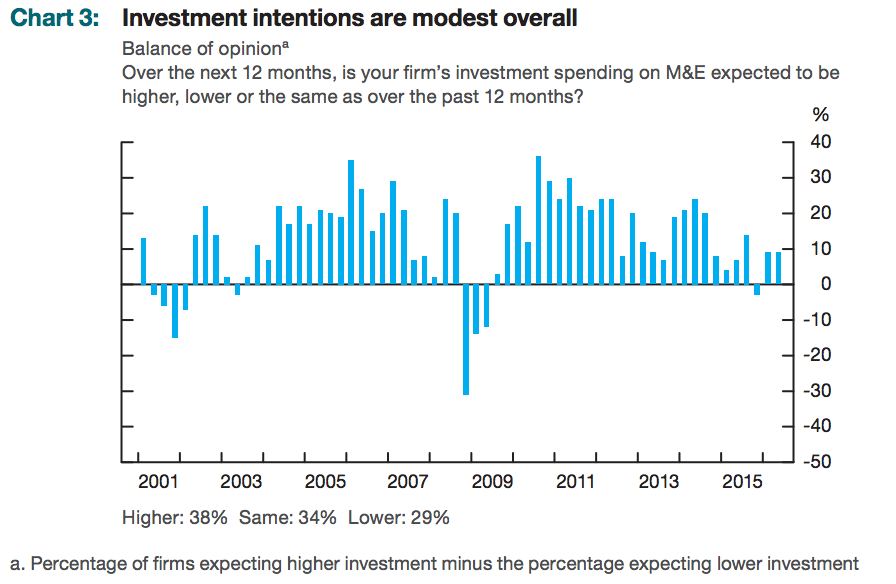

This chart from the Bank’s survey shows how weak the outlook for the next year is. It measures the percentage of companies that plan to increase their investment spending minus the percentage of companies that expect to pull back on spending.

This latest update on investment intentions doesn’t bode well for Canada’s economy. Business investment, which is crucial to supporting growth, has been in retreat for the last five quarters, and before that was stuck in neutral going back to 2012.

Here’s some context for how bad things are right now. The following chart compares business fixed capital investment—money that’s put into things such as plants and machinery—in the wake of the last three recessions (not including the two-quarter downturn that occurred in 2015, since the C.D. Howe Institute’s Business Cycle Council has not acknowledged that as an official recession). As the chart shows, this is the weakest business investment recovery since at least the early 1980s, which is as far back as Statistics Canada keeps comparable public data.

What sets this post-2008 cycle apart from the previous two is how robust the initial rebound was. For that, Canada could thank the sharp resurgence in oil prices that followed the 2008 crash as well as the boom in residential home construction. But that early surge fizzled out, and real (inflation-adjusted) business investment now back to where it was prior to the recession.

It would be easy to pin the blame for the slump squarely on the oil patch, which has scaled back plans for big oil sands projects following the oil price crash that started in mid-2014. But this is also a story of non-energy companies refusing to put their money to work. In a recent briefing report the Conference Board of Canada found that many non-energy industries—particularly manufacturing sectors like the transportation equipment, wood products, food, primary metal and paper industries—are already bumping up against capacity limits. Yet businesses in those sectors have been reluctant to invest and create more room to expand. As the Conference Board said in a statement: “The continued lack of investment has the potential to severely limit Canada’s future growth.”

Canada is hardly alone in this struggle. The recovery in business fixed-capital investment in the U.S. after the Great Recession is also seriously lagging earlier post-recession periods. When the U.S. Federal Reserve chose to hold rates in June, it specifically called out weak business investment in that country by way of explanation.

Yet there is no simple explanation for why this is happening. It’s not as if it’s expensive to borrow and invest, what with interest rates in both countries near all-time lows. And as has been pointed out, the oil crash hammered energy companies, but cheap oil and the low dollar (in Canada at least) should have spurred non-energy exporters to take advantage of those ideal conditions.

Ultimately, it comes down to confidence—or the lack thereof. Business don’t have faith that investments they make in new capacity today will provide enough of a return to justify the risks. They simply don’t believe domestic or international economies are on the mend, and the shock delivered by Britain’s decision to exit the European Union may only deepen their uncertainty. It could be some time before they get their nerve back.