The Canada bubble

The Canadian economy is booming and investors are flooding in. Is it too good to be true?

David Stobbe/Reuters

Share

Bob Haber and David Madani are foreigners who have spent a lot of time studying Canada. Haber, an American, was chief investment officer at fund giant Fidelity Canada for 12 years and tracked Canadian stocks from his base in Boston. Meanwhile, Madani, a New Zealander, spent a decade with the Bank of Canada as a forecaster and policy analyst. Both are outsiders with an acute understanding of the inner workings of the Canadian economy. That is where the similarity ends.

Last December, Haber’s new book, Go Canada: The Coming Boom in the Toronto Stock Market and How to Profit From It, hit bookstores. Haber, who now runs his own investment firm in Boston and manages a series of Go Canada funds for Toronto-based Canoe Financial, has emerged as one of the most enthusiastic proponents of Canadian investments at a time when the world can’t seem to get enough of us. With Canada’s strong economy and wealth of resources, Haber predicts the S&P/TSX Composite Index could double to 30,000 points within 10 years. “Global growth and all the free money out there are coming together and investors are realizing the best place in the G7 for them to put their money is Canada,” he says. “Things are in gear for Canada to really outperform.”

Madani’s outlook couldn’t be more different, though it tends to get drowned out amid the Canuck euphoria. Last fall, he joined Capital Economics, a prominent U.K. investment research firm, to cover the Canadian market from Toronto. He says the boom in commodities is due for a reversal. More importantly, Canada’s red-hot housing market has soared into the danger zone. By his estimates, house prices are set to plunge at least 25 per cent, and will drag the economy down with them. “Housing has gotten crazy, it’s a bubble,” he says. “These things always have an unhappy ending, and Canada is not going to be any different.”

So there you have it. Canada is either primed to be a world beater, or we’re about to go down the tubes. There’s arguably never been a time when forecasters have been so divided in their views of Canada’s economy. That’s partly due to the seemingly Herculean way we shrugged off the global recession while almost every other developed nation tanked and continues to struggle—a feat that can’t help but arouse a bit of too-good-to-be-true anxiety.

But the division of opinion has to do mostly with the two particular engines that have driven our success—resources and real estate. Both are cyclical. Prices rise and fall as supply and demand shift. Only that’s no longer seen to be the case in Canada. Never mind that some experts now say the surge in commodities exceeds anything we’ve seen in two centuries, or that by many measures the housing market sits at multi-decade highs. Those who see good times ahead are convinced the phenomenal gains reflect a fundamental shift in the global economy. In short, it requires one to ascribe to the four most dangerous words in the world of investing: this time it’s different.

As it is, the love-in for all things Canadian is in full swing. In January, giant U.S. retailer Target announced plans to take over hundreds of Zellers stores in 2013, its first expansion beyond America’s borders. The company expects big things from shoppers here; Target believes its new Canadian stores will help drive annual revenue, now around US$67 billion, to more than US$100 billion over the next few years. And Target is just one of many big name U.S. retailers, including J.Crew, Kohl’s and Marshalls, banking that Canada’s prosperity can make up for sagging sales on their home turf.

As it is, the love-in for all things Canadian is in full swing. In January, giant U.S. retailer Target announced plans to take over hundreds of Zellers stores in 2013, its first expansion beyond America’s borders. The company expects big things from shoppers here; Target believes its new Canadian stores will help drive annual revenue, now around US$67 billion, to more than US$100 billion over the next few years. And Target is just one of many big name U.S. retailers, including J.Crew, Kohl’s and Marshalls, banking that Canada’s prosperity can make up for sagging sales on their home turf.

Canada is also the toast of international think tanks and world leaders. They praise our sound financial system, which seemingly avoided the traps that engulfed other nations’ banks. Conservative legislators in America and Britain sing the virtues of our relatively sound government finances. Like a cherry on top, theEconomist magazine once again just selected Vancouver as the world’s most livable city, with Toronto and Calgary also making it into the top five.

Investors, both domestic and foreign, simply can’t get enough of Canada. In 2010, non-residents poured $116 billion into Canadian investments, the highest level ever. In January, they continued to add to their haul, snapping up $11.8 billion in Canadian securities. That month Peter Schiff, the CEO of Euro Pacific Capital and someone well known for his dismal view of the American economy, set up operations in Toronto and has been promoting the country as an ideal place to invest. “I think the Chinese appetite for resources is going to be particularly voracious,” he said in a speech from the floor of the old Toronto Stock Exchange. “Canada has a lot of what China needs.” Then, last month, HSBC, the U.K.-based banking giant, launched an exchange-traded fund devoted to Canadian stocks that will trade on the London Stock Exchange. “We think that Canada, with the relatively uncommon combination of being rich in natural resources coupled with having a stable political system, has attractive features for growth investors,” Mark Rodino, HSBC head of ETF sales in Europe, told the U.K.’s Money Observer magazine.

Eleven years into the bull market in commodities, it’s easy to forget just how much Canada has riding on strong resource prices. For one thing, the boom has boosted our paycheques. The rise in commodity prices was responsible for two-thirds of the 15 per cent gain in disposable income experienced in the last decade, Bank of Canada governor Mark Carney said in a 2008 speech. While Canada’s soaring loonie has hurt manufacturers, it’s also improved living standards by keeping inflation low. And rising commodity prices have also helped keep unemployment muted. As bad as Canadians think the recent recession was, in terms of the job market it was the mildest downturn of the last 30 years. In January, the Canadian economy added nearly double the number of jobs created in the entire U.S. economy, which is 10 times larger.

Investors have arguably been the biggest winners. The resource-heavy S&P/TSX total return index, which factors in dividends paid out to investors, has risen 120 per cent from a decade ago. That translates into a healthy annual return of 8.2 per cent, even after accounting for the roller-coaster plunge we went through in 2008. On the other hand, a Canadian investor who sunk his money into America’s S&P 500 total return index a decade ago has seen the index rise just 29.5 per cent since then. Worse still, once you take into account the soaring loonie, that S&P 500 investment is actually down 17.8 per cent, or an annual return of -1.94 per cent (after the U.S. dollar investment is converted back to Canadian currency). No wonder Americans are flocking north.

All of those benefits have fed directly into Canada’s apparently Teflon housing market. When the Great Recession hit, prices dipped briefly, but quickly rebounded as homebuyers borrowed heavily to get into the market. In fact, relative to incomes, house prices in Canada are now nearly as overvalued as they were in the U.S. at the peak of that country’s housing bubble, notes Madani.

As with soaring commodity prices, the strong housing sector has contributed in a big way to the country’s boom-time mentality and sense of invincibility. It’s been a crucial driver for labour markets. According to Madani, construction jobs account for close to 7.5 per cent of total employment, far higher than at any point since the 1970s. Meanwhile, as house prices climbed, households have been more inclined to go shopping.

But the housing boom has also gone hand in hand with Canada’s household debt boom. Over the last decade, Canadians have doubled their consumer and mortgage debt loads, to more than $1.5 trillion. For every dollar of disposable income households earn, they now carry $1.50 of debt, a level higher than in the U.S. That’s a worrying stress point that could undo the high-flying Canadian economy if it hits turbulence—in exactly the same way heavy debt loads left American households exposed. “Canada’s success story is uncomfortably similar to the U.S. success story,” says Robert Shiller, a professor at Yale University who accurately predicted the real estate crash in the U.S. “It might be offensive to Canadians, but we’re like two peas in a pod.”

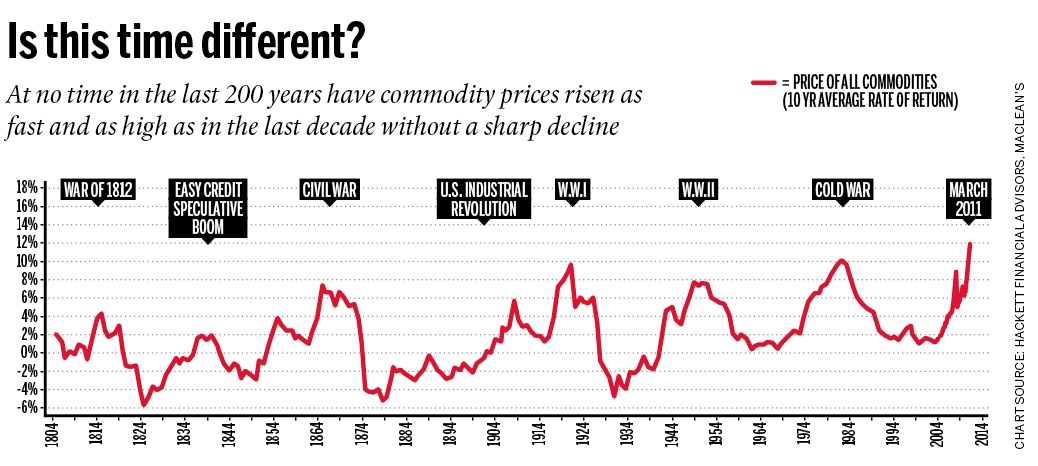

What’s different is that the U.S. didn’t have the resource sector to fall back on. But how secure should we be in assuming the commodity boom won’t turn into a bust? Not very, says Shawn Hackett, a commodity analyst in Florida who has dug into the sector’s long history of booms and busts. He analyzed the 10-year average annual rates of return for commodity prices dating back to the early 1800s. At no time have prices risen as fast and as high as they have over the last decade without being followed by a sharp decline. “If history is any guide, we’re higher than the 1980 top and much higher than the 1950 top,” he says. “Unless we are going to do something right now that defies 200 years of the way the rules of engagement have been in commodities, we’re due for a nasty spill.”

What has always happened in the past, and what Hackett expects to see again, is that as prices rise, consumers cut back while producers ramp up supply. The end result is a supply glut that drives prices back down.

Just as we’ve come to rely on rising commodity prices for our prosperity, a resource sector bear market would hit Canada particularly hard. For one thing, it could strip Canada of the cherished view we’re more prudent than other countries. After all, Ottawa and the provinces vigorously drove up spending even before the stimulus measures of 2009 were announced. It’s just that revenues, from royalty payments and corporate and income taxes, rose faster. Today, Canada’s gross national debt stands at 82 per cent of GDP, up sharply from 65 per cent in 2007 and higher than at any time since the early 1980s, according to the International Monetary Fund. (America’s rate, at 92.7 per cent, is higher, but the gap isn’t as wide as Canadians like to believe.) Canada’s debt picture is forecast to improve over the next few years, but for that to happen, the commodity and housing markets must stay strong. If resource prices plunge, Canada could be left yet again with structural deficits similar to the 1990s.

Investors would be hit hard, too. The Canadian markets have never been more exposed to the resource sector. The S&P/TSX Composite is four times as resource-intensive as Canada’s overall economy, according to CIBC World Markets. If commodity prices tank, the energy and mining companies that powered returns over the last decade could act like an anchor on investor portfolios.

But it’s Canada’s housing market, and those who have overextended themselves with massive mortgages, that stand to lose the most. The housing sector has become inextricably tied to the broader story of Canada’s elevated standing in the world. It’s a powerful and psychological link, says Shiller, who explored how bubbles form in his book Irrational Exuberance. “Bubbles are mediated by price increases and new-era stories,” he says. Any time you hear talk of a new era—such as Canada becoming the envy of the world, or that soaring commodity prices are here to stay—and it’s used to justify rising prices, it’s a good sign you’re in bubble territory. If a commodity bust does occur, one of the key foundations of the housing bubble would crumble along with it.

For now, economists remain divided on how the Canada boom will play out. Doug Porter, deputy chief economist at BMO Capital Markets, says the brief commodity market downturn in 2008 revealed how much Canada needs the resource sector to remain strong. But he argues the 20-year bear market in commodities during the ’80s and ’90s means we are only halfway through the current rebound. Likewise, Haber says those forecasting a downturn are themselves misreading history. “What Canada has are strategic resources that emerging economies need,” he says. He points to Canada’s oil sands, which are seen as a more stable source of petroleum given unrest in the Middle East, and says that supply shortages will keep oil prices high for a long time to come. “This is only the second act of a three-act play.”

On the other hand, Tom Bradley, president and co-founder of Steadyhand Investment Funds in Toronto, has been warning Canadians not to buy too heavily into the mantra that Canada is a safe haven. “People see us as a safe play on the emerging markets,” he says. “But that doesn’t mean we’re safe.” If anything, with the dollar so strong and the TSX near its all-time high, Bradley says now is the time for Canadian investors to look beyond our borders.

Perhaps there’s another reason to be anxious. Lately the term “Northern Tiger” has been used a lot to describe the Canadian economy. Given what happened to that other once-booming, now devastated “tiger,” the Celtic one in Ireland, it’s best not to get too used to it.