Hands off my housing bubble!

Tony Joe, a real estate agent in Victoria, received a predictable earful last spring when he distributed flyers that screamed: “Investors and foreign buyers want your property!” The glossy mailouts touted Joe’s connections to—you guessed it—China. “I got a lot of flack,” says Joe, who has been selling homes in the balmy Vancouver Island city for 25 years. “I got nasty emails and tweets.”

The backlash shouldn’t have come as a surprise. Nearby Vancouver was in the grips of a housing affordability crisis blamed on a flood of speculative Chinese money, and some Victoria residents feared their sleepy seaside city was about to tumble down a similar path. But then a funny thing happened. Joe’s phone started ringing and it didn’t stop. “Honestly, it was a very successful campaign for us,” he says. “There were a lot of people who said, ‘‘I know you deal with a lot of Chinese, can you sell my property?’ ”

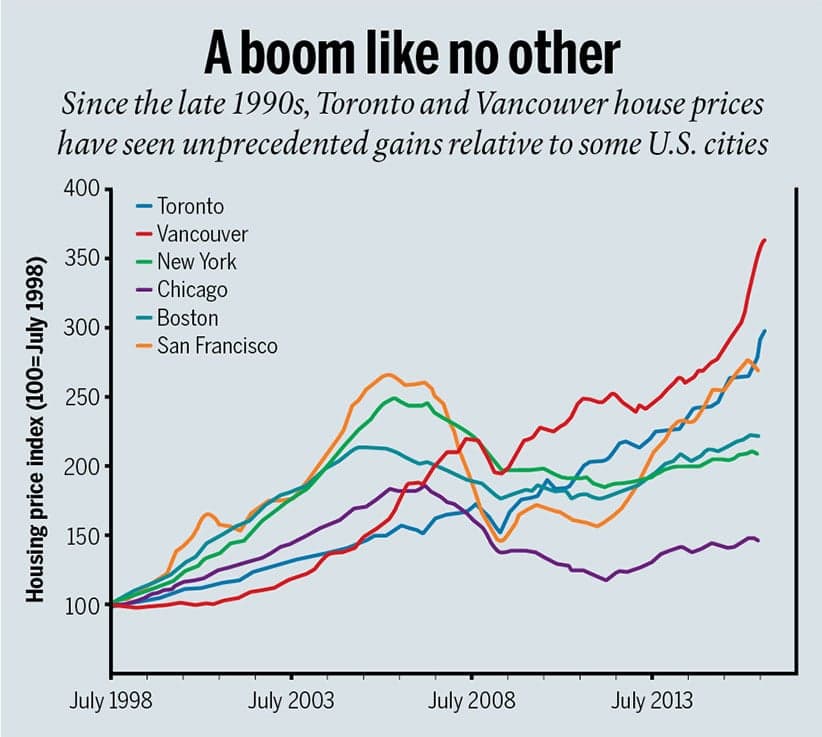

For all the outcry about mainland Chinese money driving house prices out of reach in Vancouver and Toronto, it’s easy to forget the biggest beneficiaries of the largesse have been Canadians themselves. In fact, Vancouver recently became Canada’s first “city of millionaires” as rising real estate prices—the average detached home in Vancouver costs $1.5 million—pushed average household net worth up seven per cent to just over $1 million in 2015, according to a recent study by Environics Analytics. As financial problems go, it could clearly be a lot worse.

The downside, of course, is the impact of nosebleed prices on first-time buyers. With moss-roofed bungalows selling for more than $4 million in some desirable Vancouver neighbourhoods, many local residents were understandably feeling priced out of their own city. So B.C. Premier Christy Clark’s government, bracing for an election, decided in late July to roll out an unprecedented 15 per cent tax on foreigners who purchase Vancouver houses. It worked—maybe a little too well. Vancouver house sales plummeted in August (down 26 per cent) and September (down 33 per cent) with prices expected to follow. Now some fear a painful correction could be in the works.

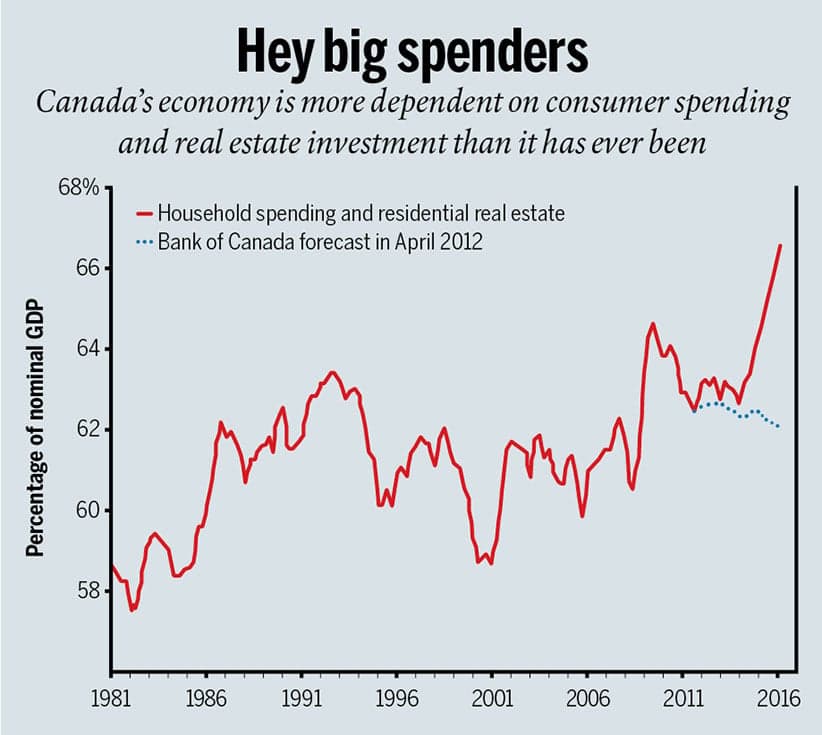

B.C.’s experience highlights the dilemma Canadian policy-makers face as the Trudeau government begins to roll out its own measures to tame the housing market. Those feeling shut out want more affordable prices. But the only way for that to happen is for incomes to grow massively or for house prices to fall. Yet, the majority of Canadians—70 per cent—now own their own homes and have built up enormous wealth, at least on paper. If prices nosedive, it will threaten their prosperity. As if this quandary wasn’t enough, politicians now face an even thornier problem: with the rest of the economy running on fumes, Canada finds itself far more dependent on real estate than ever. The housing sector—and the construction that underpins it—now ranks as Canada’s single biggest industry, comprising 12 per cent of GDP. That figure expands to 20 per cent if related industries like finance and legal services are included, and even higher when you consider the “wealth effect” of steadily rising home prices is also behind everything from sales of luxury cars to designer clothing.

Related Posts

Home Prices Are Finally Dropping

Little House in the County

Related: China is buying Canada. Inside the real estate frenzy.

Even economists who once lauded government efforts to cool housing are now expressing reservations about taking further action. “Unfortunately, the pillars of our economy have for too long been oil, manufacturing and housing,” says Sherry Cooper, the chief economist at Dominion Lending Centres. “So if you knock out that third pillar at a time when oil prices are weak, Alberta is in a recession and manufacturing is unable to replace that growth, we would have a very weak economy. There would be fewer jobs and income growth would decline.”

How did we get here? Years of relative government inaction on the housing file are one reason. Failure to grasp the potential impact of foreign money on Canadian real estate is another. But much of the blame falls on the shoulders of individual Canadians. The Bank of Canada warned for years about the dangers of homeowners getting in over their heads. But Canadians brushed off those warnings and loaded up on debt—the average household now owes a record $1.67 for every dollar of disposable income it earns. Meanwhile homeowners steadily ratcheted up their expectations of how much their house will be worth in the future when it comes time to sell it. More than one-quarter of Canadians, by some estimates, are banking on the sale of their home to fund their retirement dreams. They will understandably be furious with any elected official who, in a bid to save homeowners from themselves, inadvertently kicks their golden goose into the abyss.

If Canada’s real-estate-dependent economy follows suit, so will everyone else.

This week Federal Finance Minister Bill Morneau took the wraps off a new set of measures aimed at reining in the housing market—by far the toughest yet. Effective Oct. 17, homebuyers who put down less than 20 per cent of their new homes’ value—and are therefore required to purchase taxpayer-backed mortgage insurance—will face tougher rules to qualify for a mortgage. Homebuyers seeking a five-year fixed mortgage, by far the most popular term, must prove they can make their payments at a higher rate than those they’re being offered—usually the Bank of Canada’s conventional mortgage rate, which is currently 4.64 per cent. That’s nearly double the rate many homebuyers qualify at today. In November, there will also be changes that impact banks’ ability to access government-backed insurance for higher-quality mortgages too, making it more difficult for lenders to access funding through the Canada Mortgage and Housing Corp.’s mortgage securitization program. “Our goal is to make sure we can manage the risks in the market for the long term,” Morneau said during a press conference in Toronto, during which he seemed eager to reassure both homeowners and non-homeowners alike. “We’re looking for ways that we can ensure people’s investments in their home are stable.”

Far from making housing more affordable, the moves have the potential to limit the number of first-time homebuyers who can enter the market in the short-term. Genworth, a private provider of mortgage insurance partially backed by taxpayers, says more than one-third of insured mortgage borrowers may have difficulty meeting the new lending standards, and would have to consider buying a cheaper home or making a larger down payment.

It wasn’t all bad news for first-time buyers. Morneau also tossed a bone to those convinced foreign money is responsible for making housing unaffordable in Vancouver and Toronto (as opposed to Canadians bidding up house prices themselves by taking advantage of interest rates as low as 2.17 per cent for a five-year fixed mortgage). He promised to clamp down on what’s been described as a “loophole” in Canada’s tax laws that allows foreigners to improperly claim a principal residence exemption when selling their homes. Going forward, only people who were residents of Canada when they purchased their home will be able to avoid paying capital gains after they sell it.

Taken together, the new measures “should help to reduce the risk of a housing market correction in Vancouver and Toronto and a broader retrenchment in Canadian household spending arising from elevated debts,” wrote Sal Guatieri, a senior economist at BMO Capital Markets, in a note to clients. But as Cooper observed in a note of her own, the changes—which apply right across the country, including cities like Calgary and Edmonton where home prices are already falling—could also substantially reduce housing demand and cause prices to decline. “This, of course, is not what the 70 per cent of Canadian households that already own a home would like to see.”

Jonathan Weisman is one of those Canadians. The Vancouver lawyer sits on the board of the Dunbar Residents Association. He says he and other homeowners are “tremendously concerned” about the impact of risky new government policies aimed at promoting housing affordability on their coveted West Side neighbourhood, where a modest, 70-year-old bungalow sold for $4 million earlier this spring. Like himself, Weisman says many residents scrimped and saved to buy a slice of West Coast paradise: a detached home on a large, suburban-sized lot in a leafy neighbourhood that boasts views of Burrard Inlet, the North Shore mountains and downtown Vancouver’s forest of glass condo towers. “They shouldn’t be penalized for owning something that’s valuable,” he says.

So far, Weisman’s concerns seem justified. Whereas Ottawa took several months to develop its latest cooling measures, B.C. rushed its foreign-buyer tax into effect on Aug. 2 after collecting just five weeks of data that suggested offshore buyers, mainly from China, were purchasing one of every 10 homes in the city. The impact of the surprise move was as shocking as it was sudden: foreign nationals accounted for 13 per cent of all home purchases in Metro Vancouver in the seven weeks prior to the tax, but plummeted to less one per cent in the four weeks following. But foreigners weren’t the only ones who stopped buying. So did everyone else. “The market’s gone cold,” says Keith Roy, a local agent. He points to his neighbour’s house across the street. Worth as much as $1.85 million back in May, it was put up for sale several weeks ago for $1.8 million and the price has been dropped twice since. “It’s now down to $1.6 million,” he says. “No action.” Not to be outdone, Vancouver Mayor Gregor Robinson has announced plans to begin taxing homes that are left vacant as early as next year.

Toronto homeowners could be next on politicians’ hit list. Although Ontario Finance Minister Charles Sousa has so far resisted calls to implement a Vancouver-style foreign buyers’ tax in Toronto—at least until he has time to see how B.C.’s levy plays out—Benjamin Tal, the deputy chief economist at CIBC World Markets, argued in a recent note that Ontario has “little choice” but to follow in B.C.’s footsteps as foreign buyers swing their focus away from Vancouver. Some homeowners in Canada’s biggest city are eager to cash in while they still can. Local agent Victoria Boscariol says she now receives at least one call a week from someone with the following message: ‘‘I’ve got this property and I want to sell for a high price to the Chinese.”

To date, the discussion over soaring house prices has mostly been dominated by would-be homebuyers priced out of the market, as evidenced by a recent 200-person rally in Vancouver organized by a group called Housing Action for Local Taxpayers (HALT), and last year’s #DontHave1Million social media campaign (which should be updated to #DontHave1.3Million, based on the 30 per cent price gains Vancouver experience over the past year). But that could change if Canada’s silent majority of bubble beneficiaries feel their prosperity is suddenly at risk. “The trend toward owning versus renting has been powerful and broad-based,” wrote Tom Bradley, the president of Steadyhand Investment Funds, in a recent blog post. “So, do 70 per cent of Canadians really want to see the value of their homes go down? If a [Vancouver] West Side home drops from $2.3 million to $1.5 million, will the owner be pleased with the political leadership?”

It’s also difficult to overstate the degree to which the entire country—both homeowners and renters alike—has become reliant on rising house prices to keep the lights on. Emanuella Enenajor, a senior economist with Bank of America Merrill Lynch, says residential construction is responsible for a full third of GDP growth over the past two years. “It’s the highest we’ve had, pretty much, on record,” she says.

Rising house prices have contributed mightily to the net worth of Canadians, which clocked in at $9.84 trillion at the end of the second quarter, or $232,000 per individual. That, in turn, makes them feel richer and spend more, giving the economy a boost. According to BMO economist Alex Koustas, there’s been nearly a 40 per cent increase in sales of luxury vehicles that cost more than $90,000 over the past three years. Meanwhile, a stampede of high-end U.S. retailers, from Saks Fifth Avenue to Nordstrom, have rushed to set up shop north of the border to take advantage of a large and well-heeled, if increasingly indebted, clientele. There’s been a cultural shift, too. In recent years, Canada emerged as a centre of reality-TV programs focused on real estate, exporting no-nonsense stars like Mike Holmes and the winsome Property Brothers to U.S. audiences.

The end result is an economy where all roads lead back to home ownership. Just as the post-2009 resource boom reoriented the economy around oil production—workers left the Maritimes for higher paying jobs in Alberta, heavy equipment manufacturers in Ontario pulled back from overseas markets to focus on the oil sands—the housing boom of the last decade sucked in resources from across the economic spectrum. The number of people working as real estate agents in Toronto alone has doubled over the past decade to about 40,000. “Canada doesn’t have a lot of hard, timely information on this,” says Enenajor. “But real estate has been one of the best-performing sectors of the economy from a price and activity perspective. It would be naive to say this hasn’t had an impact on people’s choice of what kind of business they’re setting up, or the types of employment opportunities that people are pursuing.”

Governments are also held hostage. B.C. recently noted that the $2.2 billion it took in from real-estate-related taxes last year was more than it received in royalties from the mining or forestry industries. It even outstripped revenue from gambling.

What benefited from real estate’s rise will suffer if Canada’s housing boom goes bust. Avoiding such a scenario is key. But engineering a fabled “soft landing” of the housing market is like ditching an Airbus A-320 on the water. Sure, Capt. Chesley “Sully” Sullenberger piloted Flight 1549 gently into the Hudson River six years ago, saving the lives of all 155 people aboard, but there’s a reason why flight attendants joke privately about the pointlessness of all those life jacket demonstrations.

It’s unfortunate that Ottawa didn’t take more assertive steps to bring the housing market to heel back five years ago when Canada’s economy was still the envy of the world. Now, the country finds itself in the unenviable position of having to explore untested and ever-riskier measures—B.C.’s move to discourage foreign buyers is a good example—to cool house prices at a time when GDP growth is limping along at just 1.2 per cent. “It would be a very bad thing if foreigners were to sell properties in Canada, because all of us—homeowners or not—would experience a very significant slowdown in the economy,” says Cooper, who worries governments are being motivated more by political promises to help the middle class than they are by sound economic judgment.

Of course, that assumes the middle class actually wants to be protected from rising prices. Roy, the Vancouver agent, isn’t so sure. “Everybody believes in affordable housing,” he says, “until it comes time to sell their house.”

Related Posts

Inside a Salt-Sprayed Beach House in New Brunswick

The Great Unbuild

Inside a Canadiana-Themed Island Cottage

Inside an Ecohome on Stilts in Nova Scotia

Get the Best of Maclean’s straight to your inbox.

Sign up for news, commentary and analysis. Join 60,000+ Canadian readers.