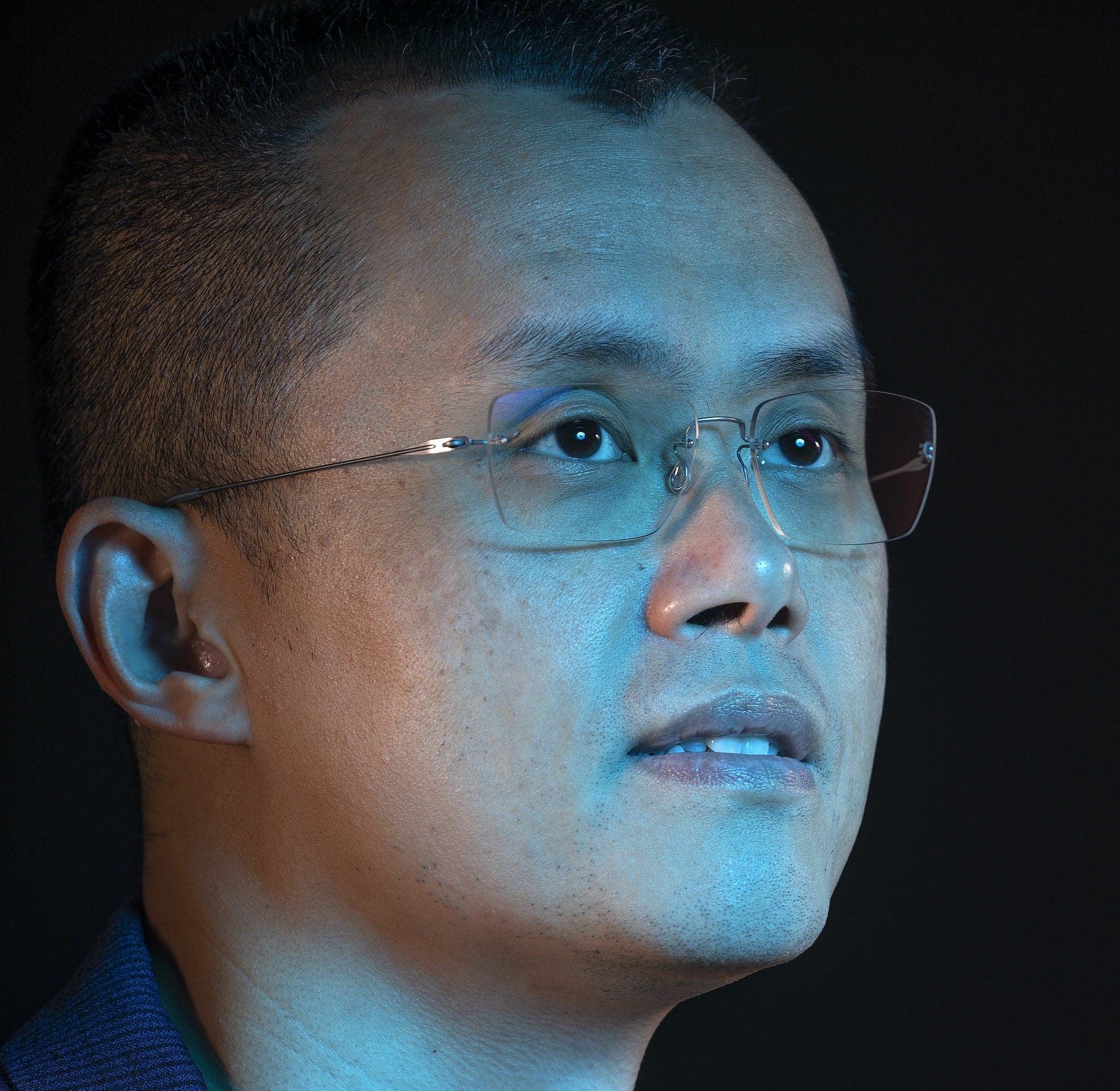

Who is Changpeng Zhao, Canada’s crypto king?

The first time I spoke with Changpeng Zhao, he was explaining the intricacies of Chinese martial arts. It was March of 2021, and I had joined the Vancouver billionaire and CEO of Binance—the world’s largest platform for buying and selling cryptocurrency—on a group audio call on Clubhouse, then an exclusive chat app. “A junior kung fu student will have a plan,” said Zhao, who is a fan of the Ultimate Fighting Championship. For Zhao, that kind of thinking is entirely too rigid. “If the opponent is dynamic,” he said, “a preset of moves does not work very well.”

Rich, successful men tend to see everything as an analogy for business. Zhao has developed an opposing tack to those newbie kung fu students, a decide-and-execute strategy that’s been an integral part of Binance’s operating model from its startup days in 2017 to now. That approach has proved profitable: last year, the exchange had 80 million users and processed nearly US$34.2 trillion in trades. This past January, Bloomberg added Zhao to its Billionaires Index in a blazing debut, with an estimated net worth of US$96 billion. A spartan man with few possessions, Zhao has disputed Bloomberg’s calculation, but it’s hard not to marvel at the number. Zhao was the richest Canadian: richer than the storied Thomson family, nearly as rich as Facebook’s Mark Zuckerberg, and richer than many small countries. He was the wealthiest man few Canadians had ever heard of.

READ: The Curious Case of Gina Adams: A "Pretendian" investigation

In the crypto world, however, fortunes can be fleeting. By the time Zhao and I spoke again in July, Bitcoin, a de facto index for the wider industry, had tumbled by almost two-thirds to a low of US$20,000, marking the onset of a so-called crypto winter. Zhao’s net worth had tumbled, too—by a reported US$85 billion. And while his company was spared from the layoffs and bankruptcies that swept the landscape, its business practices have attracted scrutiny. Binance, along with a slew of American crypto exchanges, is reportedly under investigation by the U.S. Securities and Exchange Commission, or SEC, and has otherwise tangled with authorities across the globe, including in Canada. The company vehemently insists that it runs a clean shop, but for Binance and Zhao—a man who went from virtual unknown to elusive billionaire in less than a decade—the bigger the success, the bigger the troubles.

Zhao, bespectacled and slender, was born in 1977 in China’s Jiangsu province, north of Shanghai. The Cultural Revolution ended following the death of Mao Zedong, and the country was mired in poverty and famine. Everyday citizens were regularly punished for perceived ideological crimes. Zhao’s university-instructor father, Shengkai, was branded a pro-bourgeois intellectual and exiled to a rural area. Shengkai left China to pursue a doctorate at the University of British Columbia in 1984; the rest of the family joined him in Vancouver in 1989, after the protests in Tiananmen Square. Zhao says that it was only after he arrived in Canada, at the age of 12, that he first drank fresh milk, then a rare commodity in China. During his teen years, the future billionaire took on a variety of part-time jobs—at a Chevron gas station, at McDonald’s and as a referee at volleyball games. Shengkai, a math whiz and programmer, splurged on a 286 DOS computer priced at $7,000, the equivalent of $14,000 today. The technology, cutting-edge for its time, made an impression on his son. Zhao soon enrolled in programming courses in high school and later majored in computer science at McGill University, where his father was once a visiting scholar.

Zhao’s trajectory started to crystallize in the early 2000s, after graduation: he interned for a subcontractor of the Tokyo Stock Exchange and developed trading software for Bloomberg Tradebook. As Zhao matured, so did China, which in the years since his family’s departure had welcomed economic reform. In 2005, Zhao joined other “sea turtles”—people of Chinese descent educated elsewhere—and moved back to the bustling motherland. “A couple of guys said, ‘Let’s do a startup in Shanghai,’ ” Zhao says. “So I just went.” Zhao founded Fusion Systems, an IT and business consultancy that went on to count Goldman Sachs and Credit Suisse as clients.

Related Posts

A once-bustling Greyhound rest stop sits empty. It’s a relic of a bygone era.

How these Québec-based businesses invested in energy efficiency

Zhao doesn’t have any old-fashioned political affiliations, although he does align himself with one side along a newer fault line: the “Anywheres” versus the “Somewheres.” The terms were first coined for the opposing sides of the Brexit debate, capturing the conflict between mobile globalists and those with roots in a particular local identity. “I’m definitely an Anywhere guy,” Zhao says. “Borders are just conceptual things that some people made up.”

Bitcoin was a natural fit for a man who sees himself as living and thinking beyond conventional national boundaries. Created in 2009 by an unknown entity by the name of Satoshi Nakamoto, the currency can be transferred from user to user without the involvement of financial intermediaries. Bitcoin’s community jokingly dubbed it “magic internet money,” as its underlying blockchain technology facilitated transactions as easily as sending an instant message. “We are in a much less geographically constrained world,” Zhao says. “A blockchain also doesn’t have the concept of borders, right?”

Zhao first learned about crypto during poker games with friends. According to one finance professional who explained the concept to him, Zhao’s interest went beyond simple curiosity. “He took action, you know?” says his friend, who asked to remain anonymous. “He really studied it and started looking for opportunities in that area, as far back as 2013.” By then, Bitcoin and the wider cryptocurrency universe had grown into a billion-dollar industry, much of it concentrated in Shanghai, the booming tech capital of China. Zhao attended crypto conferences and found work at emerging firms like Blockchain.com and Okcoin. He sold his apartment in Shanghai and dropped roughly US$1 million to buy Bitcoin at US$600 per unit. Zhao maintained his conviction even as property in Shanghai doubled in value and crypto’s fell by half—his first winter.

In 2017, he founded his own exchange platform in Hong Kong. Its name, Binance, was a combination of two words: “binary,” as in the ones and zeros of computer code, and “finance.” Like many other crypto businesses, it functioned like a stock exchange, matching buyers and sellers and taking a cut of every trade. Zhao seemed to have a grander vision in mind, suggested by Binance’s early motto: “exchange the world.”

When Bitcoin was invented, naturally, there were no specific laws in place for it. Authorities weren’t sure whether or how to apply existing financial regulations. Nobody said you couldn’t build a platform around magic internet money, or even make and sell your own coin. In the eyes of crypto entrepreneurs, they were free to build a new world without the usual institutional constraints. “My worldview, in most places I’ve lived, has been: if there’s no law against it, it is legal,” Zhao says. Binance’s founding was fortuitously timed: in 2017, Bitcoin surged 20-fold to US$20,000 a unit. Binance sold its own token, BNB, to raise funds for its launch, and became the go-to market for every crypto coin imaginable. But soon, China, which had so readily welcomed Zhao back, became more risk-averse. The country cracked down hard, banning some crypto fundraising and shutting down domestic exchanges. Hong Kong was only nominally a separate jurisdiction, and Binance still served users in the mainland. Zhao, who seemed preternaturally sensitive to the way the wind blew, plotted a move next-door, to Japan.

Aided by the sheer number of coins it listed—and the roadblocks now in the way of its Chinese competitors—Binance experienced an overwhelming surge in popularity. Half a year after its launch, the platform had to suspend the creation of new accounts, updating its infrastructure to accommodate the influx of traffic. Existing Binance accounts were being sold for a premium online. In January of 2018, US$6 billion flowed through the exchange in a single day. The next month, Forbes, notable for its rich lists, crowned Zhao its cover star. China wasn’t the only country trying to bring order to the field, however, and Zhao and Binance quickly outstayed their welcome in Japan. This pattern of closing up shop, setting up shop and closing shop again would repeat in places like Malta and Singapore. “Before, there was no regulation, and now there is—it happens all the time,” Zhao says. “When that happens, you’ve just got to comply. When you think it’s too strict, and there’s no business to do, you leave.”

The constant wandering of Binance, led by its nomadic CEO, known by the moniker “CZ” in crypto circles, became central to its identity. As early as 2019, the company claimed to have no headquarters. There were various Binance entities around the world—Binance Holdings Ltd. in the Cayman Islands, Binance Capital Management in the British Virgin Islands—whose individual functions were a mystery to outside observers. This untethered framework was convenient. It presented Binance as a modern firm, with staff all over the globe; it fit with the borderless nature of crypto; and in the view of Zhao’s critics, it made Binance harder to hold accountable. A 2020 Forbes article reported on the existence of a leaked tai chi–inspired strategy document allegedly crafted for Binance, aimed at thwarting U.S. regulations through a complex bait-and-switch process using various entities. (In a statement, a rep for Binance called the article’s contents “false and misleading,” and denied that the alleged third-party document was produced for or by a current or former Binance employee.)

As the company grew, it became the place to buy, sell, borrow and lend coins, and to execute particularly risky trades. Like in many other sectors, Binance’s revenues rose in the aftermath of the pandemic. Government stimulus ushered in a renewed enthusiasm for investing, and the exchange’s trading volume surpassed an astonishing US$100 billion. Earlier this year, Binance pledged hundreds of millions of dollars in two wildly expensive deals that signalled its hungry ambitions, even though they ultimately fell apart: participating in Elon Musk’s bid to buy Twitter and, separately, pursuing a stake in Forbes, the very publication that had covered Binance’s alleged plan to tiptoe, tai chi–style, around regulations.

Zhao—still not a household name—saw his net worth cross into mind-boggling territory, to the tune of US$96 billion. The amount encompassed his stake in Binance, but not his undisclosed personal crypto holdings. In other words, he was likely worth far more.

Many people became spectacularly rich in the crypto world at the time, albeit not to Zhao’s level. At its peak, near the end of 2021, the value of all cryptocurrencies ballooned to US$3 trillion. One of Binance’s rivals, the Singapore-based exchange Crypto.com, spent roughly US$700 million to rename the Staples Center in L.A. after itself. Research by the U.S. investment firm Jefferies showed that American adults under 35 were using their new cryptocurrency profits to buy art, jewellery and other luxury goods.

Zhao, on the other hand, didn’t own a house or even a car. For a man who had publicly rebuffed the notion of a fixed address, material possessions seemed to be a burden—never mind, as he put it, “parties, boats, champagne—all of that stuff.” When I asked about Zhao’s life outside crypto, his financier friend came up with nothing beyond the fact that Zhao had been excited to see Top Gun: Maverick. To Zhao, true wealth seemed to be the ability to have nothing.

In recent months, as governments increased borrowing costs to deal with inflation, all manner of investments faced decline. Bitcoin went into free fall, and crypto firms went from spending millions on Super Bowl ads and celebrity endorsements to rescinding job offers amid waves of layoffs. But Zhao didn’t flinch; he’d lived through winter before. “It wasn’t a surprise,” Zhao says. “And when it’s not a surprise, you’re slightly better prepared.”

A young, hard-to-police industry, full of riches and potential, had initially attracted the adventurous, but crypto’s volatility has a way of beating a certain humility into them. In a move that flew in the face of his supposed no-strategy strategy, Zhao had, during boom times, instructed Binance’s team to maintain a decade’s worth of operating reserves—an amount in the area of 10 figures. This rainy-day fund enabled Binance to brave this spring’s downturn better than many of its competitors; in fact, the company spent untold sums bailing out some of its troubled peers.

Zhao’s personal net worth, however, took the kind of hit that is, for some, difficult to fathom, sinking to approximately US$11 billion per the Bloomberg Billionaires Index—a US$85 billion loss. Because Zhao’s billions are largely attributable to his sizable stake in Binance, his everyday life was largely unaffected. In mid-May, after Binance’s investment in Terraform Labs’ ill-fated Luna token plummeted from a value of US$1.6 billion to less than US$3,000, Zhao took to Twitter: “Poor again,” he joked.

Binance’s ongoing regulatory tussles, though, were more serious. Within the cryptosphere, the firm had generally enjoyed a good reputation. It reimbursed users after a 2019 hack siphoned funds off the platform. (As a comparison, after the Canadian exchange QuadrigaCX collapsed in 2019, clients were out more than $200 million in crypto assets. Its co-founder and CEO, Gerald Cotten, was reported dead, and, allegedly, he alone held the passwords.)

Most of Binance’s issues were the run-of-the-mill, red-tape sort, easily kept at bay by expensive lawyers; but lately, they have been escalating. After the Ontario Securities Commission instructed crypto-trading platforms to register paperwork by June of 2021, Binance left the province. In April of this year, the Dutch central bank slapped Binance with a €3.3-million fine for failing to register, after issuing a public warning to the company just under a year prior. SEC investigators are reportedly examining whether Binance’s initial coin offering in 2017 amounted to the sale of a security, one that should have been registered with the agency. And a Reuters investigation from June alleged that Binance processed at least US$2.35 billion in transactions stemming from hacks, investment frauds and illegal drug sales between 2017 and 2021. (A rep for Binance said Reuters’ report used outdated information to establish a false narrative, and that the company has some of the strictest anti–money laundering policies in the fintech industry.)

In May of last year, Bloomberg reported that the U.S. Department of Justice and the IRS had launched probes into whether Binance had acted as a conduit for tax evasion and money laundering. There is speculation that Zhao has been avoiding the U.S. due to possible arrest—which he dismissed as “bullshit” to me. “Google, Facebook—they’re still working with regulators on data, privacy issues, different things,” he said. “It’s just very normal.” Of the more than 40 cryptocurrency exchanges that currently exist in the U.S., every one is reportedly at varying stages of being investigated.

In a case with considerable parallels to Binance’s, the crypto company Block.one had its own run-in with the SEC. It raised funds by selling its own coin, EOS, between 2017 and 2018. Despite racking up US$4 billion in sales, Block.one ended up shelling out a mere US$24 million in a settlement—without admitting or denying wrongdoing. When I asked Zhao if he sees a similar outcome for Binance, he declined to comment, though he did chuckle at Block.one’s relatively small fine. “I guess that’s a good thing,” he said.

While Binance distinguished itself in the beginning with no plan, no headquarters and no borders, Zhao now seems to understand that there are certain forces you cannot avoid, only endure. When we spoke in July, he had been spending time in Paris. Binance’s team was meeting with officials from Europe and Asia. “Today, the regulators are looking at centralized exchanges,” he said. “Once we settle that, there’s decentralized finance. What are we going to do for NFTs? Then there’s the metaverse. Even if you look at banking regulations, there are still new rules being introduced.” In the end, it was easier for him to change than the institutions. CZ has been swapping his black Binance tees for a suit, covering up the Binance logo tattoo on his forearm and drinking $14 orange juice at the Four Seasons.

Binance set up an office in Calgary toward the end of 2021, with the goal of hiring up to 75 people. Zhao also recently brought on Lawrence Truong as the new vice-president and general manager of Binance’s Canadian operations. Truong previously held positions at TD Bank and the Alberta Securities Commission, and was tapped to turn around the beleaguered Toronto exchange Coinsquare as its former chief compliance officer. “He was 100 per cent adamant that Binance was going to get licensed in every jurisdiction,” Truong says of Zhao, who has, so far, landed licences for the company in France, Italy, Sweden and Lithuania. Zhao has also obtained a residency card in Dubai, the “somewhere” where he’s decided to buy an apartment and a minivan. As for his plans to settle on a headquarters for Binance, Zhao has said that will happen very soon.

MORE: How three sisters (and their mom) tried to swindle the CRA out of millions

Some ask whether crypto is dead with the recent crash, or if it will ever be less mercurial. To Zhao, a man well used to winter, those questions aren’t of real concern. “I don’t care what the price of crypto is,” he says. “The internet is a technology for transferring information. The blockchain is a technology for transferring value.” Crypto will change our lives just as the internet did, he believes. Sure, he told me that he’s not as smart as Steve Jobs, but he also made a comparison to the iconic Apple co-founder unprompted. It’s a subconscious recognition, perhaps, of the niche that Binance occupies in the crypto world: not hugely popular among regulators, but beloved by fans with a tolerance for flux. By August, just two months after Zhao’s net worth had fallen nearly 90 per cent, Bloomberg estimated that it had more than doubled to roughly US$25 billion. In crypto, the only predictability seems to be the lack of it. “It takes a certain type of personality to deal with a lot of uncertainty,” Zhao says.

In the latter half of 2021, Shengkai died of leukemia near Toronto. Zhao didn’t return to Canada for the funeral, citing COVID restrictions. Plus, he says that the formality wasn’t all that important to the elder Zhao. “My father was the kind of person who says, ‘When I die, just take the ashes and spread them over the sea,’ ” Zhao says. He was not someone who believed in xingshizhuyi—who cared about rituals and ceremony. It was the only time during our conversations that Zhao lapsed into Mandarin.

This article appears in print in the October 2022 issue of Maclean’s magazine. Buy the issue for $8.99 or better yet, subscribe to the monthly print magazine for just $29.99.

Related Posts

The Power List

Why isn’t more clothing made in Canada?

Stephen Poloz on economic dangers ahead, staying positive and lessons from Star Trek

A Canadian company is changing the way we buy mattresses

Get the Best of Maclean’s straight to your inbox.

Sign up for news, commentary and analysis. Join 60,000+ Canadian readers.