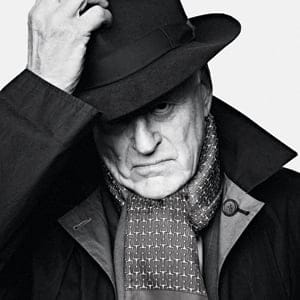

The meaning of Peter Munk

With Peter Munk about to abandon his chairmanship of the Barrick mining empire at next week’s annual meeting in Toronto, it seems only appropriate to dwell on his fall from grace. From being the invincible king of international gold mining, the pride of Canada’s business tycoonery, the talented Mr. Munk finds himself accused of having moved too far, too fast, at too high a cost—leaving his company stuck with a tricky salvage operation.

But that is not the guts of the story, not the sum total of this remarkable mega-entrepreneur’s long journey from his aristocratic Hungarian background to at least three excursions into commercial glory. That sequence of initiatives climaxed in his successful run as the world’s champion gold magnate, who until the past three years could do no wrong. The dramatic reversal of his standing on Bay Street brought into play British explorer George Leigh Mallory’s 1924 comment about Mount Everest. When asked why he risked his life climbing the mountain, he famously replied: “Because it’s there.” Sixty-four years later, on Sept. 29, 1988, when Stacy Allison became the first American woman to conquer the great peak, was asked the same question, she smiled and shot back: “Cause I’m here!”

That’s the essence of Peter Munk, explained in three words: the optimistic, fast-action guy, convinced that everything he touched would turn to gold. For most of the past five decades that was pretty well what happened. His company was flying high and he dominated its annual shareholders’ meetings, rhetorically armed to meet any challenge. It was at these public performances that he shifted into high gear, using messianic hand gestures and commanding body language. Inevitably, he won over his audiences.

At this AGM, it will be much tougher. For three years Barrick’s share value has been falling. The company has been selling off assets and taken more than $15 billion in writedowns since 2012, including the disastrous acquisition of a copper company that Barrick borrowed $6 billion to buy in 2011. (To shore up its debt-laden balance sheet it raised $3 billion in equity last year.) The Munk magic was history. His golden presence can no longer afford to float above the fray.

Worst of all, Munk, who turned 86 in November, abandoned his essential power base of loyal shareholders by initially ignoring their insistence that he reduce the outrageous compensation paid his directors and executives. Some more realistic payouts are now being contemplated, but the signing bonus of $11.9 million for John Thornton, Munk’s chosen successor as chairman, remains in place, as does the newcomer’s 2013 haul of another $9.5 million. It follows a pattern: former Barrick CEO Aaron Regent, who collected an $11-million signing bonus in 2009, got a $12-million reward for being fired three years later. (That somehow seemed out of balance; he was paid more to leave than to arrive.)

Related Posts

What Canada can learn from Germany’s mass, unplanned migration

Mark Carney sits down with Paul Wells: Maclean’s in Conversation

An internal blitzkrieg followed. At last year’s annual meeting in April, investors controlling an astonishing 85 per cent of Barrick’s shares rose up in protest by voting against the company’s approach to executive compensation. It was a serious, unprecedented condemnation of Munk’s management style, and it followed a 66 per cent plunge in Barrick’s share price since 2011. The shareholders had spoken. At the same time, seven of Canada’s leading pension funds strongly and publicly criticized the levels of Barrick’s executive payouts, protesting that they were “inconsistent with the governance principles of pay-per-performance” while setting “a troubling precedent in Canadian capital markets.” Ahead of this year’s AGM, some of Barrick’s biggest investors indicated they want to see even more changes. “If the board turns out to be completely tone deaf, I guess the board is completely tone deaf,” said Michael Sabia, the CEO of Caisse de dépôt et placement du Québec, in February. “They’ll have to live with the consequences of that.”

In the face of investor unrest, it was revealed Barrick and rival gold-mining giant Newmont Mining had hoped to announce a deal to merge ahead of Newmont’s annual meeting on Apr. 23. While the talks broke down without an agreement, the two sides reportedly still hope a deal is possible before Barrick’s AGM—a final match-up as the consummate deal-maker heads for the exit.

Munk has never thought of himself as being one of those shallow, self-made men who worships his creator. But I remember the moment during one of our many conversations, when he boasted about the extent to which the company defined his life: “Barrick is my life,” he told me, rising behind his desk. “It’s something I created. I conceived. I conceptualized. I lived. It’s a miracle not to be repeated. It will go down in the annals of business history.”

The first experience Munk and I shared was being postwar engineering students at the University of Toronto—he in electrical and me in mining. The downtown campus was so crowded with demobilized war veterans that the university had to move its engineering faculty to an abandoned artillery-shell factory at Ajax, Ont. It was there that we both started our careers: Munk’s first company employed fellow students selling Christmas trees outside 17 downtown Toronto supermarkets; I opted for journalism by becoming Ajax editor of the Varsity, the student newspaper, and had a Christmas job as assistant magician in a department store toy section. At about this time, the youthful Munk ran out of money and moved to Delhi, in southestern Ontario, to pick tobacco for 40 days on 12-hour shifts. He returned with $360.

The next time I saw him, 20 years later in 1975, he was in Toronto, following the return from his self-imposed banishment in Fiji, where he founded a highly profitable hotel chain. Things were at such a pretty pass at the time that I became his landlord, as he rented a holiday property I then owned in Caledon, just north of Toronto. He turned out to be an ideal tenant. One stormy afternoon, he phoned me with a request: “Would you mind terribly if I added a tennis court near the lake on your property?” My reply was simple: “Hell, no. Please. Be my guest . . . ”

It has never been easy to portray the shifting essence of Munk’s persona, since if he wasn’t in business, he would surely have been a professional actor—which he essentially is, just not recognized as such. He has a dozen faces, but the description that I claim for him is F. Scott Fitzgerald’s word picture of Jay Gatsby, his best-known, fictional protagonist: “If personality is a series of unbroken, successful gestures, then there was something gorgeous about him—some heightened sensitivity to the promise of life, as if he were related to one of those intricate machines that register earthquakes 10 miles away.”

Yeah, that would be Peter at his best, exercising the power of second sight that allows him to see through people and events to unexpected realities that awe his friends and disturb his enemies. But it is his dashing personality that has driven him to take impossible risks. That has meant exercising his essential life force, which, until two winters ago, included the most dangerous ski runs in the Swiss Alps where he winters. (He has worn a pacemaker since 2004, but unlike a fellow tycoon, the late Izzy Asper, he does not claim that it opens his garage door.)

That penchant for risk-taking also means Munk has never had qualms about taking public positions that go against Canadian values. Such was his glowing approval of Chilean strongman Augusto Pinochet at Barrick’s 1996 annual meeting when Munk glossed over the dictator’s blood-stained human rights record of murder and mayhem that had by then claimed a estimated 40,000 victims. In a similar comment, Munk once told me that he hired a certain director because he knew every dictator by his first name, and most of his mines were in those Third World countries.

For a time, when it meant something beyond fabulous, Munk cornered the world’s gold markets. But that was not, at least to his mind, his best deal, one he could never duplicate. That would be his Clairtone caper in the 1950s and 1960s, when Frank Sinatra became a volunteer shill for the magnificent sound systems that first put Munk on the map. They were widely advertised as: “Listen to Sinatra the way Sinatra does—on a Clairtone!” Initially manufactured in a converted Toronto warehouse and selling for slightly less than the price of new Volkswagens, the breakthrough units combined sexy Norwegian furniture with superior electronics. The company produced what was then universally recognized as the entertainment market’s most desirable luxury sound systems, featuring solid-state amplifiers. The units were so popular that most purchasers didn’t take the time to try them out in stores. They rushed home where they could listen at full volume.

Enlisting as his senior partner the debonair David Gilmour, who personified the best of the Canadian establishment ethic, to connect with society’s upper crust, the partners were riding high. Following a typically triumphant management meeting, a group that included a duo of winsome women executives climbed aboard the elevator in Clairtone’s offices. They were glowing with camaraderie when one of the women, standing next to Munk and looking intensely at him, declared that his music machines were wonderful, his vision was inspiring, and his leadership was admirable. Then, in dulcet tones, she added: “I want to make love with you . . . ”

This hardly qualified as average sales hype, so the elevator’s passengers hushed and stared at Munk, impatient to hear his reply. I wasn’t there but was told that you could watch Peter’s brain working, as he become aware of the suddenly proper alignment of the stars. He smiled at the lady beside him, tilted his head, and smoothly cooed: “That’s OK for you,” followed by a drawn-out pause: “But what’s in it for the company?” Vintage Munk.

Munk has a dozen faces. His expressions seldom change but his appearance shifts with his moods. One moment he looks as confused as an usher at a shotgun wedding, 10 seconds later he claims the magisterial bearing of a pope presuming worship. Same guy; different mood. Those who know him most intimately—all three of them—swear he is a false extrovert, aggressive and demonstrative when the occasion requires visible strengths. More often, he is remote and private, his countenance betraying journeys across some pretty lonely, risk-strewn terrains. He has been at the top and he has been at the bottom, absorbing equally both experiences.

His current difficulties would unnerve a lesser man, but at heart he’s still a Hungarian. And that, as most Europeans attest, is a very special state of grace. It is commonly rumoured Hungarians define themselves by entering revolving doors behind you, and coming out ahead of you.

But always, whenever our formal interviews petered out, he would return to what he still considers to have been his most profound business failure. “Clairtone was my first love,” he begins, his voice a mournful monotone, decades after the firm collapsed, having overextended itself. “It was my first infatuation with the romance of business. It was unrequited, it was immensely uncompleted, and that’s why it made such a major impression on me. But it was an experience that formed the foundation of everything that I have accomplished in my life.”

In fact, it was the classic, impossible dream. During our subsequent private conversation, the lesson he claimed to have learned was never again to give away his destiny, and not to become so far removed from day-to-day relevancies that the exercise of control passed out of his hands.

Yet that was precisely what happened all over again at Barrick when its shareholders voted overwhelmingly against him. It was the long-forgotten reminder of what money manager Ira Gluskin once called “the Munk discount,” based on Peter’s alleged deficiencies, often cited but never proven.

Out of the catharsis that followed the Clairtone trainwreck, there emerged the hard core of Munk’s character. It took most of several decades for him to acquire enough confidence to fuel his new ventures, though his motives were never as innocent or as uncomplicated as minting money. It was his bitter feeling of not being appreciated for what he had accomplished that motivated the Peter Munk epic—the three great motivators in Peter Munk’s life, I wrote at the time: restitution, redemption and revenge. It was about giving the finger to all those snotty guys from Upper Canada College and Harvard’s business school who never waved goodbye as he departed for his exile in the South Pacific after the Clairtone fiasco back in 1967—and didn’t welcome him back with a tickertape parade when he returned.

He returned to Canada from that excursion with $110 million in his jeans, or so he told me. I was suitably impressed. But when he called on the Royal Bank to sign up for a promised investment, they made him wait for an hour beyond the appointed time—then sold him a minor, insolvent gold mine. At the time, not a single broker took notice of his return. These were undeserved slights for a quintessential Canadian tycoon with more than his share of successful incarnations.

Before the current troubles, Munk won much of the acceptance he so coveted. He’s received two tiers of the Orders of Canada (officer, then companion)—having each time been so moved by the ceremonies that he cried through most of the proceedings. His thoughtful choice of philanthropies has successfully bolstered his image. Until recently, the verdict of Bill Wilder, the former head of the once-powerful Wood Gundy and one of Bay Street’s most esteemed establishment figures, was right on target: “Peter Munk is well respected because of the superb jobs he did with Barrick and Trizec, and nobody can take that away from him. But he’s never going to be one of the boys playing poker at the Toronto Club. He’s a cold-blooded, tough Hungarian who is going to paddle his own canoe.” Munk has since not only joined the Toronto Club, he became the first Jew on its management committee. Predictably he never lingers for the club’s afternoon poker jousts.

When you ask Peter Munk about his corporate philosophy, he looks around in case he might be overheard, then confides: “I don’t want to be a guy everybody likes. I want to do what looks impossible.” And that, precisely, is his problem. Consider his Pascua Lama mine project, which is so huge and costly that Barrick’s future swings on it. It was his biggest gamble. He tested the limits of the possible and found them wanting. The stunning gold strike straddles the Chilean-Argentine border, a shared jurisdiction where the problems started.

For starters, the gold deposit is high up in the forbidding Andes Mountains, which is a difficult place to work because it is always much too hot or much too cold.

Munk had originally planned to invest slightly more than $1 billion to finance an open-pit gold mine near the top of the mountain range. Small problem. It turned out that part of the gold field was located under glaciers. The original Munk strategy was to, well, transport the ice to nearby storage. The volume to be moved kept growing, eventually reaching 830,000 cubic meters.

The glaciers weren’t the only stumbling block. There was a land-ownership court battle. And the area’s 70,000 farmers in the nearby Huasco Valley feared for their water supply and Barrick offered to distribute $60 million in social assistance. Meanwhile the Chilean government imposed 400 conditions on the project. Costs ballooned to more than $8 billion. The project is currently suspended. Barrick has already taken a $6-billion impairment charge—a fate all too similar to another Barrick project, the Lumwana copper mine in Zambia, which saw the company take a writedown of $5 billion in 2012, a year after purchasing the mine.

Munk’s next move will invariably follow a pattern established over a half-century in business. Just as he did when Clairtone cratered, he will reappear in another incarnation, this time as the silk-scarf-tucked-into-blazer admiral of a fleet of mega yachts docked at Porto Montenegro, once part of Yugoslavia, on the Adriatic Sea. There, in 2006, he acquired a semi-abandoned former military port, which he is converting into a new Monaco. (That used to be his favourite port of call until, while swimming off his boat one sunny Sunday afternoon, a used condom floated by and brushed his knee.) Munk’s response was buy the Montenegran harbour, with partners.

No longer a gold bug, he has transmogrified into the guiding spirit for the wealthiest of Europeans who will dock their floating palaces at the more than 600 yacht berths that will eventually be available. His own super-yacht, the Golden Eagle, is 40 m long, manned by a permanent crew of five.

It may seem sad that Peter Munk, whose genius and hard slugging built Barrick into such an impressive big-league player in the world of mining, leaves on a down note. Not to worry. In 1991, the last time I learned the details of his pay packet, he was taking home a cozy $32.6 million. Last year, when Barrick reported a loss of $10.4 billion, Munk still pocketed $3.9 million. Now that’s chutzpah.

Related Posts

The ’safe bets’ and ’wild cards’ needed to meet Canada’s net zero emissions target

Capitalism’s connection to our ever-worsening mental health

The working class has had enough

What Canada’s economic recovery might look like

Get the Best of Maclean’s straight to your inbox.

Sign up for news, commentary and analysis. Join 60,000+ Canadian readers.