![IMPORTANT CHARTS_TILE_2[1]](/_next/image/?url=https%3A%2F%2Fmacleans.mblycdn.com%2Fuploads%2Fmac%2F2014%2F12%2FIMPORTANT-CHARTS_TILE_21.jpg&w=640&q=80)

The most important charts for the Canadian economy in 2016

If a picture is worth a thousand words, a good chart has just as much capacity to inform our understanding of the world. Which is why Maclean’s has once again asked dozens of economists, analysts, investors and financial writers to each share their pick for the most important chart for Canada in the year ahead. The charts cover the full range of factors impacting our economy, from trade and energy to demographics and employment. And next to each chart you’ll see a brief explanation from each person about why they believe the chart is so important.

After looking at these charts, it’s your turn. Do you have a chart you think will be important for Canada in the year ahead. We want to see it, and know why you think people should watch it. Send it to us on Twitter, on our Facebook page or link to it in the comments section below.

Now read on, and enjoy.

Click on each chart to open it in a new window. For best viewing on mobile, turn your device to landscape.

Canada needs oil prices to reboundDawn Desjardins, RBC economic research"The drop in oil prices in the second half of 2014 resulted in a 30 per cent drop in investment by energy companies in 2015 with the weight being sufficient to drive the economy into negative growth territory in the first half of the year. A rebound in export activity starting in June combined with firm consumer spending and housing market activity likely skated the economy back into the positive column in the third quarter. Looking to 2016, oil prices are expected to firm modestly as supply is reduced and becomes more closely aligned with demand. However this will be a gradual process and prices are likely to remain in the lower end of the range in place over the past decade. At these levels, Canadian energy companies are expected to reduce investment again, albeit by less than half 2015’s drop in percentage terms. Failure of prices to recover raises the prospect of even deeper cuts to investment by oil and gas companies next year and would likely result in Canada’s economy remaining on a slower growth path than the 2.2 per cent pace we are expecting."

A stronger loonie aheadDavid Rosenberg, Gluskin Sheff and Associates"Oil prices used to have an 80 per cent correlation with the loonie and now it is a 94 per cent relationship. Further the commodity looks to have not just carved out a bottom but is visibly basing — the U.S. production and inventory data have finally become supportive. But what is key is that finally, the cheaper currency has triggered a manufacturing revival. All roads lead to a firmer loonie until otherwise notified."

Fewer rich people ahead?Lindsay Tedds, University of Victoria"The new Liberal government has promised to quickly implement its promise to raise the statutory tax rate on incomes over $200,000 from the current 29 per cent to 33 per cent. This represents the first federal increase to the highest income tax bracket since the federal income tax system was reformed in 1988. In addition, in the provinces of Alberta, Newfoundland, and New Brunswick, these earners are also facing increases in the provincial statutory tax rates that are being implemented at the same time. Some have argued that these high-income earners will flee the country to avoid this steep rise in tax rates or engage in tax avoidance measures to shelter their income. In addition, the provinces of Alberta and Newfoundland are increasingly affected by the drop in oil prices that has resulted in layoffs. This has led others to suggest we might see a reallocation of high-income earners across the provinces as they seek employment in those provinces less affected. Overall, these conditions suggest that there might be some change to the proportion of persons reporting income above $200,000, particularly by province."

More inequality in the slices of the economic pieMiles Corak, University of Ottawa"Globalization and the computer revolution have changed the way Canadians work, how much they earn, and the inequality in their incomes. The share of total market income going to richest tenth has risen, while the share going to the bottom 40 per cent has fallen. The top is richer and more secure, the bottom has stagnated and life is more uncertain. At the same time, the ability of middle and upper middle income groups to maintain their slice of the pie—getting more education, putting off marriage, having fewer kids, working harder—has led to more stress, time pressure, and an unease about what comes next. But this chart is as interesting for what it doesn’t show: nothing beyond 2011. We should look forward to Statistics Canada coming to the plate with a more up to date picture of how the economic pie is shared."

A needed bounce in exportsCraig Wright, RBC economic research"The combination of the weakness in energy weighing on investment along with high levels of indebtedness keeping consumer spending modest puts the weight on the external side of the economy to much of the lifting of growth in the period ahead. The combination of a recovering U.S. economy and the more competitive currency are showing early signs of a bounce in exports, a trend that is needed to continue in the year ahead for overall economic growth to accelerate."

Ontario, the problem provincePhilip Cross, Macdonald-Laurier Institute"For decades, households in Ontario had incomes as much as 20 per cent above the Canada average, and 10 per cent higher as recently as the turn of the century. A steep decline over the past decade culminated in Ontario incomes falling below the national average for the first time ever in 2012. The struggling Ontario economy is a major reason why Canada seems stuck in the slow-growth lane of economics."

The return of the American tourist to CanadaJP Koning, Moneyness"This is a chart of overnight cross border traffic flows over the U.S.-Canadian border with the exchange rate overlaid on top. As the loonie rises relative to the U.S. dollar more Canadians flow into the U.S. while fewer Americans visit Canada. As the loonie falls, the converse happens. While the loonie began to decline in earnest in 2013, the number of Canadian visitors to the U.S. minus American visitors to Canada only began to follow in 2015. In 2016, expect increasing visits by Americans to buoy the Canadian tourism industry for the first time in over a decade and domestic retailers to benefit as Canadians stay at home. This is one of the advantages of a having a floating exchange rate. By attracting foreign buying, the weak loonie cushions some of the negative impact of plummeting commodity prices."

Provincial debt on the riseStephen Gordon, l’Université Laval"One of the challenges facing governments of all levels is going to be financing the costs of providing services to a population that is aging rapidly. After peaking in the mid-1990s, public debt steadily declined, but jumped up again during the financial crisis. The federal government has since regained control of its debt, and its debt-to-GDP ratio is almost back to pre-crisis levels. The newly-elected Liberal government plans to run deficits over the next few years, but they have assured us that these deficits will be small enough so that federal debt-to-GDP ratios will continue to fall. However, provincial debt continues to increase. In 2015, federal debt was surpassed by provincial debt for the first time in Canadian history, and this trend shows no sign of slowing."

The fallout from falling resource wagesTodd Hirsch, ATB Financial"Employees in Alberta’s petroleum sector are the highest paid in the country—and even with the current downturn, paycheques for those workers are still more than double the Canadian average. But there’s good news and bad news.

The good news is that wages in Alberta’s resource sector are falling like a stone. Compared to the recent record high peak set in April 2014 ($2,295 per week), average earnings are down nearly 10 per cent. That is helping rebalance expenses in the petroleum sector, for which payroll costs account for roughly 70 per cent of total operating expenses. The weakness in the petroleum sector is not just Alberta’s problem—it’s Canada’s problem. Oil and gas exports are among Canada’s largest, and the industry extends both directly and indirectly across the country.

The bad news is that wages in Alberta’s resource sector are falling like a stone. In Alberta alone, the loss of employment (down about 17 per cent) combined with falling earnings has yanked about $100 million per week in total household income. That’s about 3.8 per cent of Alberta’s total. This will continue to create a drag on Alberta’s (and Canada’s) macro-economy as retail, residential housing, and personal service sectors will be affected."

Foreign buyers in the Canadian housing marketDavid Wolf, Fidelity Canada"This is a chart of purchases of Canadian residential real estate by non-residents. Yes, it’s blank. These purchases are not measured in Canada. That needs to change. Circumstantial and anecdotal evidence suggest that these capital inflows have had a large and growing influence on the Canadian housing market, whose imbalances continue to represent a key risk to the Canadian economic and financial outlook."

Canada’s economy is heavily exposed to housingBen Rabidoux, North Cove Advisors"As a percentage of GDP, investment in residential housing in Canada hit 25-year highs last quarter. Not surprisingly, employment in the construction industry, which historically has tracked residential investment, also sits near all-time highs. The previous peaks in housing investment preceded the real estate downturns in the late 70s and late 80s, as overbuilding ultimately led to excess supply. Of particular concern, working-age population growth is running at just a third of the long-term average, meaning the current housing boom lacks the robust demographic underpinnings seen in previous cycles. Perhaps this time is different, but should housing investment and construction employment return to long term norms, it could result in some 250,000 lost jobs in the sector."

Many households don’t have financial safety netsJennifer Robson, Carleton University"This is a spider graph from the 2012 Survey of Financial Security (Statistics Canada) showing the incidence of ownership of certain kinds of assets by household income quintile. It’s from a study I did this year commissioned by Prosper Canada. Semi-liquid assets here refers to equity in a principal residence (also broken out on its own), locked-in retirement savings and pension assets — financial assets that are imperfectly liquid. To me, this is a peek at the safety nets of households in different income groups.

The high income households have nice broad, diversified safety nets that can allow them to withstand shocks (oil prices, housing prices, employment fluctuations, unexpected illness) by shifting through short, medium and long-term forms of saving. They also are far and away more likely to have the kinds of assets (home equity, TFSAs, RRSPs) that benefit from favourable tax treatment. On the other hand, the lowest and modest income households have much narrower personal safety nets. A sudden shock can mean they quickly blow through their cash deposits and have no medium-term semi-liquid savings. To borrow the phrase from Michael Barr’s book, they have no slack. Given softer economic projections and a more volatile global economic environment, we need to be paying more attention to household differences in assets and resilience."

Canada needs stronger business investmentGlen Hodgson, Conference Board of Canada"2015 was another mediocre year for the Canadian economy, growing by only 1 per cent in 2015 after a technical recession in the first half of the year. The weakest aspect of Canada’s economy this year was the feeble performance of private investment, projected by the Conference Board of Canada to contract by nearly 8 per cent compared to 2014 levels. Much of this contraction is due to the sharp pullback in investment in the oil patch, now expected to decline by 40 per cent over the course of the year. That result for 2015 is depressing enough—but as the chart shows, Canada’s poor private investment performance in 2015 was not a one-time thing.

There’s more to this story than just low oil prices as Canadian firms continue to sit on mountains of cash embedded in their balance sheets. As a result, it is no surprise that we are in the midst of a multi-year period where growth in private investment is weak—the lagging edge of our economy—with little sign of a significant turnaround in 2016. A prolonged period of little or no real growth in private investment is bad news for productivity growth, since it suggests we are missing opportunities to invest in new technology, build our productive base and boost the competitiveness of the Canadian economy. What could prompt stronger investment growth? The growing U.S. recovery should boost demand for Canadian exports and eventually cause firms to invest in order to expand their productive capacity and seize the available export opportunities. But until there is evidence that Canadian firms are responding to a stronger order book, private investment will remain the lagging edge of our economy."

Millennials will support house prices, for nowSal Guatieri, BMO Capital Markets"The chart shows yearly growth in the number of Canadians aged 25 to 34—the millennials—including Statistics Canada’s projection. This cohort of prime first-time home buyers will continue to underpin housing demand for a while. So, Toronto and Vancouver’s high-flying markets could remain hot in 2016, especially if interest rates stay low and foreign wealth continues to pour in. But it will likely be a different story next decade when this age group starts shrinking, as occurred in the 1990s when the baby boomers approached middle age."

The full impact of the oil shock has yet to be feltDavid Madani, Capital Economics"Oil prices have fallen to levels that are no longer profitable for many energy producers. With no end in sight, producers are slashing their long term investment plans. After averaging $70 billion in 2014, oil and gas investment could fall to as low as $40 billion in 2015 and even lower in 2016. This sharp decline in investment is worth 2 per cent of GDP, with the full force of this shock across the country likely to be felt in 2016."

A decision on renewing the inflation target is imminentFrançois Dupuis, Desjardins Group"In fall 2016, the Bank of Canada, in cooperation with the Minister of Finance, will decide whether or not to change the country’s inflation target. Since 1991, Canada’s annual inflation has averaged 2 per cent while its variability has diminished by two-thirds. This system of inflation targeting has been very beneficial for the overall economy. However, since the financial crisis ended, interest rates have been much, much lower, leading to more episodes of key rates hovering near zero. This suggests that an inflation target greater than 2 per cent should be considered, like they have in Australia (between 2 per cent and 3 per cent over the entire economic cycle). Another possibility is to widen the fluctuation band from 1 per cent to 4 per cent with still a target at 2 per cent. However, the solution currently being reviewed—that of having certain negative rates, like in some European countries—adds another possibility to the next decision by Canadian monetary authorities. To be continued..."

The changing face of Canadian exportsTrevor Tombe, University of Calgary"Oil prices began their decline in late 2014, and show no sign of rebounding. The implications for Canada’s economy are often overblown, but they aren’t trivial. Energy exports have declined substantially through 2015, from over one-third of exports at the beginning of 2015 to just over one-quarter today. In 2016, non-energy exports are projected to account for almost all export growth and energy exports will remain flat. Trade matters to all Canadians in all regions. The changes will be good for some, and less so for others. We should all watch this data with interest."

Canada’s urban economic enginesLivio Di Matteo, Lakehead University"There are six Census Metropolitan Areas (CMAs) in Canada that stand out when it comes to employment levels and job growth. Montreal, Toronto, Vancouver, Ottawa-Gatineau, Calgary and Edmonton are marked by the distinction of being the only Canadian CMAs where total employment is greater than 500,000 jobs. As of late 2015, employment ranges from a low of 767,100 for Edmonton to a high of 3,212,300 for Toronto. The next highest cities after these six are Quebec City at 447,700 followed by Winnipeg at 428,000 – both still yet to reach half a million jobs. The Big Six CMAs are Canada’s economic engines and their share of total Canadian employment has grown steadily from 44 percent in the mid 1990s to reach 49.3 percent by October 2015. Since 1996, employment in the Big Six has grown by 49 percent while employment in the rest of Canada has only grown by 23 percent. In 2016, expect these CMAs to reach 50 percent of Canadian employment marking a new era of urban economic development in Canada. Half of all Canadian jobs will be in these six urban areas."

Expectations for Canadian growth are rising George Pearkes, Bespoke Investment Group"Over the last 15 years, the difference between the five year government bond yield and the overnight Bank of Canada rate has been a reliable indicator of the trend growth in the Canadian economy. As shown in this chart, since 2010 the two are almost identical. This makes sense; lower growth should result in bond yields falling, anticipating lower Bank of Canada rates in the future and less need for a risk premium around inflation. Since bottoming below zero (an "inverted" yield curve) back at the beginning of this year, the combination of higher five year yields and BoC rate cuts have sent this yield spread higher. If the market is right, that suggests Canadian growth should rebound into the end of 2015, putting the technical recession earlier in the year in the rear view mirror. Happy days may not have arrived again, but markets are certainly getting more optimistic about the outlook for the Canadian economy than they were to start 2015."

Canadian exports depend on U.S. demandDanielle Goldfarb, Conference Board of Canada"As a relatively small economy, with relatively weak economic growth prospects, Canada depends on trade to boost or even maintain our living standards. Rapid growth in emerging markets led to soaring commodity prices and grew Canada’s exports to China and other emerging markets in recent years. But as emerging market growth moderates, we can no longer ride the commodity supercycle and we expect weaker growth in Canada’s trade outside the U.S.. Canadian companies will need to think beyond natural resources. This could include, for example, high-value services such as engineering and computer services in which this country already has global expertise. Fortunately for Canada, the U.S. economy is rebounding. Canadian companies that have invested in their capacity and labour will be well-positioned to take advantage of growth in U.S. demand."

The regional shift in employment will continueDoug Porter, BMO Financial Group"This chart in nutshell captures the rapidly shifting economic fortunes between regions as a result of the oil shock, the Canadian dollar’s steep drop and the ongoing improvement in the U.S. economy. The latter two are big supports for the Ontario economy, while the former is obviously a massive drag on Alberta. In turn, the deterioration in Alberta was so significant this year that it pushed up the national unemployment rate, and was the primary factor behind the drop in Canadian GDP in the first half of the year. With oil prices dropping anew and now testing the $40 level, it looks like this massive regional shift will dominate the Canadian economic landscape again in 2016. Note that Alberta’s jobless rate has been higher than Ontario’s in only one month since 1990 (June 1994)."

Government’s share of GDP has shrunkKevin Milligan, University of British Columbia"Questions about the ultimate size and role of government lingered in the background in 2015 policy debates ranging from pensions to childcare to infrastructure. The answer will depend on one’s views on the competence and efficiency of government actions over different kinds of economic activity. But the debate should be informed by fact—and the fact is that government’s share of economic output has shrunk over the last 20 years."

The housing market is in line with employmentWill Dunning, Mortgage Professionals Canada"We hear lots of commentary that Canada is over-producing housing relative to demographic requirements. But, over time housing starts are usually not even close to the estimates of demographic requirements. Rather, housing activity follows the economy, especially the employment situation. During the post-recession period, the share of Canadian adults who have jobs has been relatively high in historic terms. Correspondingly, housing starts have been relatively high in historic terms. The housing market is producing the outcomes it should, given the economic conditions that exist."

Inflation risk has risenDerek Holt, Scotiabank"Inflation risk is likely to limit further policy flexibility at the Bank of Canada at least for some time. Stabilizing commodity prices will gradually stop exerting downward pressure on inflation. Further, over 60 per cent of the “core” Consumer Price Index that excludes more volatile items is posting gains of 1.5 per cent or more and one-third of the basket exceeds the Bank of Canada’s 2 per cent inflation target. For how long a weakening Canadian dollar raises import costs and whether risks to the housing market intensify will take time to evaluate in terms of consequences to inflation risks. This connotes a likely period of low short-term interest rates."

Housing is affordable at the national levelLarry MacDonald, author"Will 2016 be the year the Canadian housing market finally collapses? This is an important question to ask not only because housing tends to be the biggest asset for most Canadians but the sector is also a major driver of booms and busts in the Canadian economy. While certain housing markets, like Vancouver and Toronto, do seem frothy and at risk of some kind of correction, the Bank of Canada’s Housing Affordability Index suggests a bust is not on the horizon at the national level. As of mid-2015, the measure (see blue line in chart) shows that less than a third of disposable income is required by a representative Canadian household for mortgage payments and utility fees–below the long term average (brown line). Side note: The affordability measures from Royal Bank of Canada show housing to be less affordable but they use posted mortgage rates whereas the Bank of Canada uses discounted mortgage rates."

Lower oil prices worse than initially fearedStephen Tapp, Institute for Research on Public Policy"When oil prices fell sharply 1½ years ago, people wondered how bad the shock to Canada’s economy might be. What if oil stayed at just $60 a barrel for a few years, as the Bank of Canada assumed in January 2015 when it cut interest rates? The Bank even included a grimmer ‘what-if’ scenario with oil flat-lining at $50 — this figure shows how bad that might be for Canada compared with no oil price drop. Throughout 2015, oil price have actually been closer to this $50 ‘worse case’ than the $60 assumed when rates were first cut. In 2016, economists will be watching whether global economic growth and oil prices rebound. If not, painful regional and sectoral adjustments will continue in Canada. Low interest rates only do so much, different policies are needed to encourage new investment in Canada, reallocate capital and labour within the economy and raise our slowing potential output growth."

What happens to house prices if rates don’t go any lower?Martin Pelletier, TriVest Wealth Counsel"The six-city Teranet National Bank House Price Index is estimated by tracking the observed or registered Canadian home prices over time which we’ve compared to the inverse of the Bank of Canada overnight lending rate. As you can see there is a strong relationship between the two as ultra-low interest rates have provided underlying support to the housing market especially in 2015 with two Bank of Canada rate cuts.

Looking ahead, one has to wonder if there is room for lower interest rates and what will happen to the housing market in 2016 in a flat rate environment - especially in Alberta where there are ongoing layoffs. This is important given the impact housing has on the overall Canadian economy whereas a robust housing market increases consumer confidence which is a significant component of the nation’s GDP. In particular, real estate is the largest component of household wealth accounting for approximately half of all total assets. Fortunately, while debt levels are rising they have not kept pace with the growth in real estate prices across the country - at least for now anyway."

A tale of two economiesBarry Schwartz, Baskin Wealth Management"2015 was hardly the best of times for Alberta and Saskatchewan, but the underlying strength of Ontario and Quebec helped prevent Canada’s economy from sinking into a deeper recession. The precipitous drop in the price of oil had a calamitous effect on Alberta and other energy intensive provinces, so consumers in those regions were in no mood to shop, buy cars or new homes. However, improving commodities prices in 2016 will help restore confidence and Canada will get back on track to sustainable growth over the long term. A country that works together, grows together."

Progress toward gender equality has stalledTammy Schirle, Wilfrid Laurier University"Because it’s 2015. This most simplistic statement refers to one of the most difficult and intangible policy problems. In the private sector, Canadian women working full time are earning hourly wages that are 80 per cent of what men earn. A large part of the wage gap reflects occupational segregation. In the natural and applied sciences, only 22% of private sector full time employees are women. Looking to our future, only 34 per cent of economics majors at the Lazaridis School are women. Change is remarkably slow, but I keep looking for it."

The importance of growth in GDP per personMichael Veall, McMaster University"Growth in per capita GDP will not just improve the individual standard of living but it is the best way to balance government books. Without increasing the tax share of output, 1 per cent real growth over the next 40 years will yield an inflation-adjusted increase in tax revenue per capita of about 50 per cent. With 2 per cent growth, that increase is 120 per cent, 70 percentage points more. That extra money will be necessary to try to meet the ever-increasing costs of our healthcare and pension systems."

A world awash in debtBrett House, Alignvest Investment Management"In response to the 2008 global financial crisis (GFC), most advanced country governments rightly undertook debt-financed spending to prevent economic activity from collapsing. Seven years on, their collective real debt is the highest recorded since the 1830s—even higher than the peaks reached to finance the first and second World Wars. Canada’s federal government is in relatively good shape, though its debt would balloon if a province were to default. Some other countries are much more likely to have trouble servicing their debt as global growth continues to slow. Sovereign debt crises tend to be messy and drawn-out—as Greece has shown—because the world lacks a global bankruptcy process to restructure debts that governments can’t pay. When the next wave of public debt distress hits foreign governments, Canadian investors, borrowers, and exporters will all be affected."

The rise of federal government debtAaron Wudrick, Canadian Taxpayers Federation"For all the talk of a falling "debt to GDP" ratio (a metric that politicians love to use because it doesn’t require them to actually pay down any debt) our federal debt continues to rise, and now stands at over $612 billion. Last year debt interest charges alone were $26 billion, which represents a considerable opportunity cost. With the new Trudeau government pledging more deficits, public debt and cost to service it appear set to keep growing for the foreseeable future."

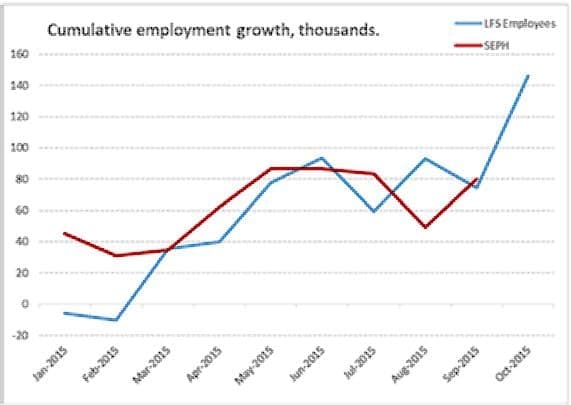

Two different stories of Canada’s job market healthDerek Burleton, TD Bank"Employment is a key barometer of the performance of the economy. Yet Canada’s two main measures of job creation released by Statistics Canada -- the Labour Force Survey of households and the employer-based Survey of Employment, Payrolls and Hours. (SEPH)-- have been moving along very different paths in recent months. The former more closely-watched data have pointed to steady and healthy job gains in 2015 while the latter indicator has struggled to post even negligible growth. These two surveys have tended to track each other in the past, so the question becomes which one is telling the true story? Our sense is that in light of the oil shock and weak economic growth recorded in Canada this past year, the SEPH is likely telling the more accurate story, meaning we could see employment as measured by the LFS slow significantly during the first half of 2016."

* Note: Statistics Canada’s response to this chart has been added to the end of this post.

Oil production has yet to reflect lower pricesMike Moffatt, Ivey Business School"After the sudden decline in oil prices in the second-half of 2014, some thought that oil production would be cut in response. This has yet to happen in any meaningful way, as both OPEC and non-OPEC countries have seen their production increase by a million barrels a day since then (to 33.9 and 46.8 million barrels per day respectively), with much of the OPEC increase coming in the last few months. Economic forecasters in Canada will be watching oil production numbers closely. As long as production levels stay high, the outlook for oil prices will remain weak, as will the Canadian dollar, the TSX and the job prospects for those in Alberta and Newfoundland and Labrador."

All roads for interprovincial-migration led to AlbertaJock Finlayson, Business Council of BC"This chart highlights the outsized role that Alberta has played as a destination for interprovincial migrants in Canada since 1995. Over the past two decades, Alberta has gained almost half a million people (net) as a result of in-migration from other provinces. The only other province in the plus column over that period was BC (+69,000). Every other province experienced net outflows of people on a cumulative basis. With Alberta mired in recession and the energy industry stuck in what looks to be protracted slump, one wonders how the national labour market will be affected. It is hard to imagine that other provinces will be able to step forward to ‘replace’ Alberta, in a quantitative sense, as a desired destination for working-age interprovincial migrants looking for better economic opportunities."

The demographic outlook for housing isn’t goodFrances Woolley, Carleton University"In 2015, Canada crossed a threshold. For the first time in our nation’s history, there are more seniors 65 and older than children under 15, and the gap between the two will widen for years to come. These two groups—seniors and children—are the future of the housing market. As they get older, seniors exit the market—one way or the other—while children grow up and enter. By 2035, there will be millions more “future home sellers” than “future home buyers.” Immigration at the present level of about 250,000 new permanent residents per year will fill the gap between sellers and buyers at the aggregate level. But immigration alone will hardly keep the construction industry in the style to which it has become accustomed. And what will happen to housing prices in areas immigrants find unattractive? What will municipalities do when their property tax base evaporate? The value of principal residences, on paper, accounts for more than a third of the total wealth held by Canadian households. But that value only becomes real when a buyer signs on the dotted line. And the years when buyers outnumbered sellers will soon be gone."

Slowth is the new growthArmine Yalnizyan, Canadian Centre for Policy Alternatives"Canada’s economy is 11th largest in the world, but is growing more slowly over time. We are not the only nation facing this reality. The red line shows an overall downward trend in the rate of economic growth since 1981. The more detailed yellow trend line shows that every recession/recovery cycle since 1981 has delivered slower rebound growth. The "serial disappointments" of actual growth in recent years have caused the Bank of Canada and private forecasters to almost continuously downgrade the outlook for growth since the spring of 2013. These trends are about to collide into population aging. Statistic Canada says 18 per cent of baby boomers are over 65. Not all are retired. As the share of non-earners in the population accelerates, growth will slow even more. How Canadian decision-makers choose to address the new economic and political reality of slowth (slow or no growth) will shape our future."

Canada needs stronger non-energy exportsAvery Shenfeld, CIBC World Markets"With the energy sector still challenged by soft global growth and oversupply, and the upside in housing construction now limited, Canada needs to see a rotation towards non-energy exports. Services can play a role, but in the goods sector, we’re going to need to rebuild capacity shed after the recession and the period of Canadian dollar overvaluation from 2010-13. So far, we’ve seen ongoing declines in capital spending by non-energy firms, and we expect only limited progress in 2016. Unfortunately, it will take a longer period under a weak exchange rate, and better global growth, to make much headway on this front. Watch for data on capital spending intentions from Statistics Canada in the new year, as well as major corporate announcements."

What will it take to get businesses investing again?Jim Stanford, Unifor"Capital spending is the most important engine of economic growth. Whether by private firms or by government, capital investment generates multiple and cascading economic benefits: spending power and job-creation in the short-run, productivity and innovation in the long-run. But Canada’s investment record has been chronically disappointing. Despite expensive cuts in corporate tax rates, private business investment never really recovered after the 2008-09 recession—and some key components (like machinery and R&D spending) continued to fall. Public stimulus investments in 2009 and 2010 filled the gap for a while, but then deficit-fearing governments turned off the tap in 2011. More recently, shrinking private investment was the key factor in Canada’s “technical recession” last year. Looking forward, Canada will need a turnaround in both components of capital spending to escape its current macroeconomic doldrums. The new federal government pledges to boost infrastructure investments, but will it be enough to offset continued weakness in private capital spending? And what will it take to get Canadian companies to start spending the $700 billion in idle liquid assets currently on their balance sheets?"

Canada’s housing market faces a day of reckoningHilliard MacBeth, Richardson GMP"Most Canadians are unaware of the degree of over-investment in residential housing. Total investment is $120 billion annually, split equally between renovation and new housing. This pace is unsustainable and the adjustment will be painful."

Manufacturing’s sluggish recoveryPaul Boothe, Ivey Business School"I will be watching the growth of manufacturing sales to see if we surpass 2000 total this year. Also, I am wondering if the export share will recover? This will be a critical sign for the future health of the sector."

The pain of lower oil pricesEmanuella Enenajor, BofA Merrill Lynch Global Research"Falling energy prices sliced Canadian GDP growth in half in 2015 and triggered two rate cuts by the Bank of Canada. Looking ahead to 2016, the economy’s fate will largely be driven by the trajectory for energy prices. The oil price is already at a level that is discouraging any new investment in oil sands. If the price of energy falls further into the $25-$35/bbl “danger zone,” cash flow pressures could hamper production, leading to another wave of economic weakness."

Canada’s aging, just not as fast as some othersJack Mintz, University of Calgary"The world is aging, especially in the West but also Brazil, China, Russia and many others. The economic implications will be profound with more competitive international labour markets and the need to adopt technologies and policies to encourage people to work longer. Savings will decline as retired folk tend to consume rather than build assets, potentially leading to more competing demands for capital and higher interest rates. Governments will find their tax capacity decline as the aged population earns less income and spends less after retirement, putting pressures on governments to cut public spending or increase taxes on younger populations, the latter hurting competitiveness. Like other countries, Canadian public policy will need to adapt to this new global competitive environment arising from demographic changes. This includes recognizing that people will be retiring by choice at later ages, requiring public policies that do not incentivize early retirement, which will be increasingly viewed as too early at 65 years."

The rental market remains tight in hot marketsSherry Cooper"Rental vacancy rates are a leading indicator of housing activity, especially in the condo sector. What is noteworthy about this chart is that rental vacancy rates have skyrocketed in those regions where the oil price rout has hit the hardest—Alberta, Saskatoon and Atlantic Canada. In these provinces housing has slowed—sales, construction and prices are down. But, note that in the hottest markets—Vancouver and Toronto—rental vacancy rates remain extremely low and even fell in Vancouver, despite huge condo construction activity. This shows that these markets are not overbuilt, although I do believe housing will slow in these two cities in 2016."

Global GDP is slumpingBob Hoye, Institutional Advisors"The graph of global nominal GDP runs from 1981 to date and covers another "new era" of financial manias. Our era has been fabulous as reckless adventurers have dominated financial markets as well as central banks. As with previous examples, the action has been mainly in financial assets with real estate prices soaring in the financial centres. Although the experiment in ambitious policy has seemed without limit, there was a severe setback in 2009. The alert to the "Great Recession" was classic. Credit spreads reversed to widening in June 2007 and commodities reversed to weakening in June 2008. The rest as the saying went, was history. At -5 per cent, the current slump in global GDP is almost as severe as the one in 2009. This was preceded by the reversal in credit spreads and weakening commodities that began in June 2014. Central bankers have been charged with preventing contractions. This diminishes perceptions of risk and accounts get leveraged. Throughout history margin clerks have always trumped central bankers. This time around, central banks are highly leveraged."

A long-term perspective on stocksPreet Banerjee, author"Incessantly, you’ll hear statements like, ’The market dropped over 200 points today!’, or ’Canadian stocks are rallying, with the TSX up over 150 points!’. Without knowing the current index level, such statements are sloppy. Decades ago, those statements would’ve been big news: a 200 point move when the index was at 1,000 would be 20 per cent. Today, they are normal daily fluctuations, as a 200 point move today is closer to 1.5 per cent. Far more meaningful are framing market moves in percentage terms. A 2 per cent move today has the same significance as a 2 per cent move 50 years ago.

We often see the same sloppiness in long term stock charts. If you use the usual arithmetic (linear) price scales, the recent past looks a lot more volatile compared to the distant past. By using a logarithmic scale instead, you can easily compare the significance of vertical moves at any point along the chart. This logarithmic chart of the S&P/TSX Composite Price Index (and appropriate precursors) goes back to 1920, adjusted to October 2015 dollars. What stands out is just how volatile The Roaring 20s and subsequent Great Depression were, even compared to The Great Financial Crisis. You’ll see that there’s really nothing different about the last 20 years versus the previous 60. The market is almost machine-like from a long-term perspective."

Subnational debt is becoming unsustainableRob Gillezeau, University of Victoria"Coming into 2016, Canada’s federal and subnational (e.g. provincial, territorial, local, and indigenous) governments carry a similar net debt as a percentage of GDP. However, over time subnational debt levels will increase in an unsustainable manner. And according to the PBO, fiscal room available to the federal government exactly offsets the fiscal gap faced by the provinces. The federal government will have the opportunity to address this imbalance in the coming year through the negotiation of a new Health Accord, a major federal commitment to childcare, a federal-provincial carbon pricing framework, or other means."

The market outlook for crude is weakAndrew Leach, University of Alberta"When I submitted my recommendation for the chart to watch in 2015, I submitted last year’s version of the accompanying chart, and I believe it remains a crucial chart to watch for 2016. Since last year, the near-term price of WTI crude, in Canadian dollars, has dropped by almost $25 per barrel, and the long-term futures price by $10, when you take into account futures market prices for Canadian dollars as well. Continued weakness in the price of oil seems likely, as signaled by OPEC’s failure in December to agree on a production ceiling. This weakness will put additional pressure on provincial budgets in Alberta, Saskatchewan and Newfoundland and Labrador as well as on the federal budget. Furthermore, with no signs of recovery, the likelihood of a more profound shock to Alberta’s economy grows—the economy continues to rely on oil sands projects for which construction began before the downturn, but those projects will gradually come to completion over the next 18 months or so. If we don’t see recovery in crude prices by then, things will only get tougher out west."

The Canadian and U.S. economies have never been more desynchronizedDavid Doyle, Macquarie Canada"Canada’s residential investment is highly elevated as a share of output. In contrast, in the U.S., residential investment is low as a share of output. The difference in these two ratios has never been greater and as a result the Canadian and U.S. housing investment cycles have never been more desynchronized. With housing a tailwind for U.S. activity and a potential headwind for Canadian activity, we believe Canada is in for a prolonged period economic underperformance with the result being an even lower loonie for several years."

Surging uninsured mortgages a risk to financial stabilityDavid Watt, HSBC Canada"Based on current growth rates, outstanding uninsured mortgages could exceed insured mortgages by the end of 2016. Seemingly, despite home prices having continued to rise at a brisk pace, more and more Canadians are making down payments that are large enough (at least 20% of the purchase price) to avoid having to take out mortgage insurance. Though the recent increase in uninsured mortgages seems in part a response to rising mortgage insurance premiums, it also likely increases the risks to financial stability. The risks are heightened to the degree that vulnerable, non-prime borrowers are using funds borrowed from smaller or less well-regulated lenders to make larger down payments."

* Response from Elton Cryderman, chief of the current labour market analysis section at Statistics Canada about the chart "Two different stories of Canada’s job market health."

Related Posts

The ’safe bets’ and ’wild cards’ needed to meet Canada’s net zero emissions target

What Canada can learn from Germany’s mass, unplanned migration

When comparing the data from LFS and SEPH it is important to take into account the conceptual differences between the two surveys. One major difference is that LFS data represents employment, which includes self-employment, while the SEPH data is about employees, which excludes the self-employed.

To get a more accurate comparison of the two surveys, it is important to use the LFS estimate of the number of employees (found in CANSIM Table 282-0089), which is more directly comparable to SEPH (although there remain some minor conceptual differences). Once you use the LFS estimate of employees, the data from the two surveys track more closely, and your graph would look like this:

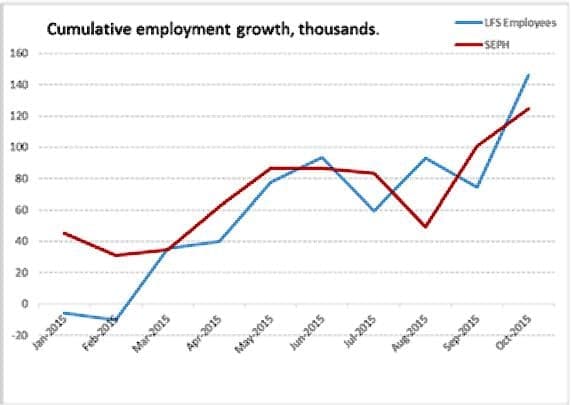

Using similar concepts between the two surveys, the September cumulative data is fairly similar between the two surveys.

In addition, October data are now available for SEPH as of yesterday, as well as revised September data. With the revised September data, and the addition of the October data, your graph would now look like this:

As you can see, the employee level data since January tracks fairly well between the two surveys. Additionally, on a year-over-year basis (October to October), SEPH employment is up by 126,500. The number of employees measured in LFS is also up by 126,000.

Jason Kirby is a Toronto-based editor and journalist. Follow him on Twitter: @jason_kirby

Related Posts

Mark Carney sits down with Paul Wells: Maclean’s in Conversation

What Canada’s economic recovery might look like

Capitalism’s connection to our ever-worsening mental health

The working class has had enough

Get the Best of Maclean’s straight to your inbox.

Sign up for news, commentary and analysis. Join 60,000+ Canadian readers.