Thought the real estate market couldn’t get any crazier? Think again

Robert Ellis purchased his two-storey house in Toronto’s Leaside neighbourhood 14 years ago. He was drawn to the area’s leafy streets, sturdy, double-brick 1930s-era homes and the proximity to local merchants on nearby Bayview Avenue—the proverbial "butcher, baker and candlestick-maker," as he calls them. But the idyllic existence was shattered in 2012 when the bungalow next door sold for $760,000. The buyer, who appeared to be acting for a developer, planned to tear down the one-storey structure and build a much larger house to be sold at a significant profit—a feat made possible by the double-digit increases of Toronto property values in recent years.

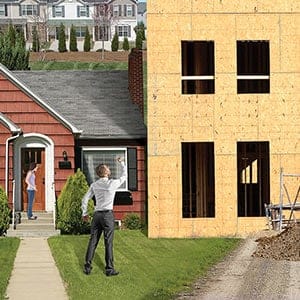

Ellis, a lawyer, wasn’t thrilled with the idea of living next to a construction site, but was prepared to make the best of it—until he saw the sheer size of what was being erected. "You’re talking about something that was 800 or 900 sq. ft. being replaced by a house that has 1,250 sq. ft. on each level—and it’s a three-storey house," he says, adding that the new home failed to comply with numerous bylaws. For instance, the design of the house was too big for the lot, and the first floor was too high above grade. Equally troubling, the mishmash of architectural styles, best described as "McDonald’s revival," clashed with the neighbourhood. And so Ellis poured "hundreds of hours" into fighting the project, enlisting the help of his neighbours. The feud hit a low point when, after noticing an odd smell one winter, Ellis discovered a one-metre column of frozen urine by his house—courtesy of the developer, who hadn’t bothered to rent a portable toilet. "I think builders are the ones making out like bandits," says Ellis. "They’re buying for what’s essentially lot value and then building these very large homes. They can make hundreds of thousands in profit and they don’t have any stake in the neighbourhood. They just don’t care."

But those living next door to or near monster homes certainly do. The soaring price of real estate—the average price for a detached home in both Toronto and Vancouver now tops $1 million—has led to a frenzy of reconstruction in many cities as owners and developers rush to capitalize on Canadians’ insatiable demand for homes. In Toronto, some 375 homes have been torn down so far this year according to city statistics, a 67 per cent jump from five years ago. John Filion, a Toronto councillor whose ward is close to Ellis’s home and has seen scores of demolitions approved this year, says the bulk of his week now consists of fielding complaints from residents about teardowns and making sure builders follow the rules. "We’ve always had new houses being built, but there wasn’t the frenzy that you’ve seen the past few years," says Filion. "Virtually every small house in the ward that goes up for sale gets torn down." In Vancouver, meanwhile, where monster-home mania is a point of even greater tension, city council recently tried to clamp down on the practice by making demolitions more expensive. Yet the move has had little impact in a city where buyers regularly plunk down millions on homes without even bothering to step inside to look around. In a sure sign of the times, there’s even a new Vancouver-based reality TV show called Game of Homes, on which teams compete "to save rundown houses that are marked to be torn down."

The debate over teardowns and unseemly builders is driven by homeowners who want to preserve the aesthetics of the neighbourhoods they bought into, but always lurking just below the surface is fear over what monster homes or new condo projects might do to property values. A huge chunk of Canadians’ assets are tied up in real estate (roughly 35 per cent in principal residences and another 10 per cent in second properties), and their value has exploded. Some $1.7 trillion in net new wealth has been created from Canadian real estate since 2000. In fact, a growing number of Canadians expect their home to pay for their retirement. Is it any wonder, then, that with so much at stake, emotions run high and disputes turn ugly? "Real estate is seen as a commodity in scarce supply—while there’s actually a lot of it out there, it’s scarce if we can’t afford it," says John Andrew, an adjunct assistant professor who studies real estate at Queen’s University. "It’s inevitable that you start to see these conflicts. It tends to bring out the worst in people."

It’s not just battles over monster homes. While bidding wars have become an unwelcome rite of passage in the quest for home ownership in Canada over the past decade, the battles have grown even more irrational and vicious of late as buyers compete for the privilege of owning dilapidated, inner-city homes that often need to be gutted to be saved. As for those priced out of the housing market altogether, there are growing calls for politicians to do something—anything—to bring down the cost of owning a home in Canada. That’s led to a NIMBYish dispute in Calgary over legal basement suites and quasi-xenophobic discussions in Vancouver about the need to clamp down on foreign property buyers—read: mainland Chinese. One local urban planner has even dubbed Vancouver a "hedge city," suggesting its single-family homes are little more than a place for wealthy foreigners to park their cash.

Related Posts

Home Prices Are Finally Dropping

Inside a Canadiana-Themed Island Cottage

RELATED: Can families still afford Vancouver?

With all the rage, greed and animosity, the country’s already overheated housing market has hit yet another level—one where desperate, would-be buyers clamour, wild-eyed, for a slice of the action, while existing homeowners go to extreme lengths to protect their property nest eggs. Meanwhile, the rest of the world looks on and wonders: Has Canada gone crazy?

In many Canadian cities, the brawls begin the moment prospective buyers set out to look for a new home. David Fleming, a Toronto realtor, says this spring is by far the zaniest he’s seen when it comes to buying a house in Canada’s biggest metropolis—and not just because most houses are attracting multiple bidders and selling for well over the asking price. "We’re seeing the bully offers take over, and it’s chaos," Fleming says, adding that he’s been involved in 20 bully-offer deals so far this year, about triple the number he saw last spring. For those unfamiliar with the tactic, a bully bid occurs when a buyer registers an offer shortly after the house is listed—usually well above the asking price—instead of waiting around for an offer night, when all interested buyers are supposed to submit bids. It’s basically the real estate equivalent of a shock-and-awe military campaign, and it’s a sign that buyers are frustrated by the blind bidding wars that are now common. "In theory, your offer has to be so incredible that [the seller] just has to take it," Fleming says. The result is that the stressful process of buying a house in downtown Toronto has gone from being a week-long affair—from the moment it’s listed to the day offers are made, including a two-day open house on the weekend—to several hair-raising hours. "A house comes up for sale on Tuesday, and the sellers say they’re going to take offers next Monday, but we all know we have to get in there tonight, otherwise it’s going to sell to the bully," he says.

Bidding wars aren’t just a Toronto phenomenon, of course. When oil prices were shooting past US$100 a barrel, there were stories of people buying properties in Calgary they hadn’t even seen. Bidding wars have returned with a vengeance in B.C.’s Lower Mainland, where one West Vancouver house recently sold for $1.1 million over its $2.98 million asking price. There are even bidding wars breaking out in Windsor, Ont., and Hamilton—a city that was once known mostly for its smoke-belching steel mills and its perennial inability to land an NHL club.

In yet another sign that buyers are losing their patience, the Real Estate Council of Ontario plans to introduce new regulations July 1 that are meant to crack down on so-called "phantom offers." That’s when unscrupulous agents hint to potential buyers that they have another offer that doesn’t actually exist in the hope of extracting more money. Under the new rules, agents won’t be allowed to suggest or imply that they have another offer unless it’s signed and delivered. "We all used to dread buying a new car, but now that experience pales in comparison to buying a house," says Andrew. "You go into the process with your back up, with a great deal of suspicion and distrust, including of your own [real estate] agent in a lot of cases."

Of course, real estate agents also have a vested interest in making the whole process seem as adversarial as possible. Bidding wars tend to quickly inflate home prices in neighbourhoods—and the commissions earned by agents—because most buyers look at the most recent sales, or "comparables," when preparing their offers. All it takes is one frustrated couple to bid $100,000 over asking on a property to turn a street of $500,000 homes into $600,000 ones. Toronto lawyer Michael Kril-Mascarin calls it the "stupid premium," meaning how much extra buyers are willing to pay to get into the Toronto real estate market. "When people have lost a couple of places already, they’re at the point of ’Screw it,’" says Kril-Mascarin, who’s lost his fair share of bidding wars, including one on a house with no kitchen and graffiti-covered walls that still drew 19 offers and a selling price of $601,000. "Banks are willing to lend, and money is cheap, so they’re offering crazy money, in my opinion."

Some analysts are inclined to agree. Ben Rabidoux, president of North Cove Advisors and a noted housing bear, says Canada’s real estate market has essentially become a tale of two cities, where Toronto and Vancouver are seeing "ridiculous" levels of activity that’s masking weakness almost everywhere else in the country. In turn, Rabidoux argues that lenders are flooding the two markets with cheap money that’s helped to drive up prices. "You’re going to try to cram volume into the strong areas like Vancouver and Toronto by competing really hard for rates and terms in those areas," he says. "That’s why it’s extremely easy to get a mortgage in Toronto right now and a little more challenging in Alberta."

The numbers speak for themselves. The price to buy a detached home in Canada’s largest city soared 18 per cent to $1.12 million in May from the year before, according to the Toronto Real Estate Board. The price for a similar home in Vancouver rose by a similarly eye-popping 14 per cent to $1.1 million during the same period, according to the Real Estate Board of Greater Vancouver’s "benchmark" price, although the figure doesn’t quite capture the city’s nuttiness because it includes several suburbs. A detached home on Vancouver’s desirable west side, for instance, is more likely to cost upwards of $2.5 million.

Unaffordable house prices have, not surprisingly, created considerable angst among Canadians and are fuelling conflict between the real estate haves and have-nots. Existing homeowners are eager to protect the vast wealth they’ve amassed on paper, while those struggling to gain a toehold on the property ladder—mostly young people—see an unfair system that rewards those who got in first.

The simmering animosity between the two worlds boiled over last month when a group of midtown Toronto homeowners dedicated to fighting "density creep" complained to the Toronto Star about a condo project being proposed for their neighbourhood. The developer planned to knock down eight older brick homes on Keewatin Avenue, which sit across the street from several high-rise apartments, and replace them with 80 stacked townhouse units. The homeowners said they had concerns about the project’s adherence to the city’s planning rules and seemed eager to stop the encroachment of multi-family buildings into their neighbourhood. But the protest quickly went off the rails when the Star quoted one homeowner as saying her main concern was the impact on the value of her house—a sentiment many homeowners might share, but seldom utter aloud. "Right now, all the houses are $1.1 to, say, $2.2 [million] but they’re looking at putting in places that are only $500,000," said the woman, who has lived on the street for 19 years.

The reaction on social media was swift and vicious. Many said the group were NIMBYs of the worst kind because they were not only trying to block development but also seeking to keep people with less money out of the neighbourhood. The irony is that the angry homeowner likely bought her house for far less than the condos she now fears will decimate her property’s value. "#DensityCreep squad, bravely defending the homes they bought at [the] equivalent of $200k when the economy was booming," wrote one Twitter user. Another tweeted it was "like a story from The Onion [a satirical news site], but in real life." Even Matt Galloway, the affable host of the CBC’s popular Metro Morning radio program, chimed in by tweeting: "What does Toronto hammering NIMBYism look like? Have a peek at #densitycreep." The group later apologized for the comments and stressed their issue was with developers, not residents who might live in the new condo units. But the damage was already done.

The same soaring prices that started a class war on Keewatin Avenue are also threatening to rip apart neighbourhoods where there are no condos in sight. The tear-down-and-rebuild trend under way in several Canadian cities is mostly driven by homeowners’ need to justify their giant investments. Put another way, since the cost of construction tends to be relatively fixed in most cities, rapidly appreciating property values encourage the construction of bigger houses since the payoff will theoretically be that much larger down the road (if prices continue to rise). It’s not unlike the questionable philosophy that underpins most home renovations—the idea that spending $30,000 on a new kitchen will magically increase the value of your home by $100,000 or more.

The formula has led to some odd sights across the country. In Winnipeg, the smaller character houses on shady Montrose Street are now punctuated by a hulking black box of a house that resembles a towering ocean liner trying to squeeze itself into a tiny marina. In Ontario, meanwhile, residents of a Brampton neighbourhood are fighting a similar battle against a monster home that looks like a big-box store plopped onto a suburban lot. Mississauga, a city of large suburban homes if there ever was one, recently passed a so-called "McMansion tax" that will charge homeowners more based on how much stormwater runoff their properties deliver to the local diversion system.

Yet, few cities can compete with Vancouver when it comes to tearing down and building bigger. By some estimates, the city is on track to issue 750 demolition permits this year alone—not an insignificant number when you consider there are fewer than 50,000 houses in the city of Vancouver proper. The situation is so bad that Mary Ann and Ian Carter did the unthinkable and bypassed the highest bidder, and sold their Dunbar house for just over $2 million (this is Vancouver, after all) to a young family who promised to leave the Depression-era home standing. "There have been three teardowns on the same side of our block," Ian Carter explains. "The whole complexion of the neighbourhood is changing." His wife adds that she simply couldn’t bear to see their quaint home razed and replaced with another cavernous new build. "We emailed our son-in-law to tell him what we were doing," she says. "He emailed back and said: ’You’re nuts.’"

The episode highlights the considerable tensions that exist under the surface in some of Canada’s most highly sought-after neighbourhoods. Rising property values make everyone on the street richer. But the gains often come at the expense of ruining the character and livability of the neighbourhood—usually the things that made them desirable places to live in the first place. Mary Ann Carter says the neighbours who’ve torn down and rebuilt on her block are usually pleasant enough, but most now rarely step outside of their castle-like homes. There’s no need to.

The trend also tends to enrage heritage advocates and those who can no longer afford to live in the city. Several community groups have begun referring to smaller houses in expensive neighbourhoods as mere "demo bait," and a quick perusal of the Vancouver Vanishes page on Facebook, dutifully maintained by writer Caroline Adderson, offers a glimpse at what the city has already lost: hundreds of perfectly habitable homes, many of them quite charming. Amid the growing outcry, the city at last adopted new rules that force owners seeking to demolish a character house built before the 1940s to reuse or recycle 90 per cent of the materials, which makes a teardown more expensive and time-consuming. Of course, in a city where a tired bungalow on the west side can fetch over $2.4 million, many are skeptical that raising the cost of demolitions by a few thousand dollars will save all those decorative turrets and soaring gables. Says Andrew: "If you’ve spent a great deal on the lot, it makes sense to have as much house as you can have."

With many Canadians feeling priced out of their cities, there have been growing calls for policy-makers to do something to bring the market back into balance. Vancouver, for example, has embraced the concept of laneway housing to increase the density of some inner-city neighbourhoods without dramatically altering their look and feel. The tiny homes tend to be about 550 sq. ft. in size and are tucked behind the lots of bigger single-family properties. Other cities, including Toronto, have explored the idea of more mid-rise development—generally condos—along major transportation corridors. But nothing is ever as straightforward as it initially seems.

In Calgary, for example, city councillors have been fighting for years over proposals to allow homeowners in more neighbourhoods to legally rent out secondary suites built in their basements, backyards or over garages—a change many other municipalities have already embraced. Proponents, including Mayor Naheed Nenshi, argue legal suites are necessary to create safe, affordable housing options in a city notorious for its sprawling suburban neighbourhoods of single-family homes (it also helps homeowners take on bigger mortgages because they can rent out their basements). However, many local residents fear that opening the doors to more "transient" renters will ruin the character of their communities. With politicians deadlocked, council recently asked city staff to look into the cost of holding a referendum on the issue, but was advised against it since it would cost as much as $2 million if held as a stand-alone vote and provide relatively little useful new information. One newspaper columnist described the experience of observing the never-ending debate as "torture."

Even those who have tried to bridge the real estate gap have found themselves embroiled in controversy. In Vancouver, a new 19-storey high-rise being proposed for city’s west end would offer a combination of affordable housing and market-rate units, as per the city’s official development plan. The problem? The two groups of residents would access the same building from different entrances. Developers say it’s necessary to keep the two parts of the building separate because they are managed independently with different finishes and amenities, but furious critics have dubbed them "poor doors," arguing they build economic segregation into the city’s infrastructure.

The closest Canada has so far come to a real-estate-related uprising took place last month when several hundred people descended on the Vancouver Art Gallery to protest the high cost of home ownership in the city. The demonstration grew out of a Twitter campaign launched by Eveline Xia, 29, a lifelong resident of the city who has a master’s degree in forestry and environmental science. Coining the #Don’tHave1Million hashtag on Twitter, Xia warned that many highly educated young professionals like her—doctors, lawyers, engineers—may be forced to leave the city if they can no longer afford to live there.

Inevitably, any discussion of Vancouver’s stratospheric house prices turns to the influence of flush foreign buyers, particularly from mainland China. David Ley, a professor of geography at the University of British Columbia and author of "Millionaire Migrants," says there’s no question that foreign money has played a significant role in influencing the Vancouver real estate market, as it has in other Pacific Rim cities like Hong Kong, Singapore and Sydney. "It’s an open and closed case," he says. "We have a city with modest incomes, but a housing market that’s priced way higher then anywhere else in Canada." He blames Canada’s so-called "millionaire visa program," designed to lure wealthy investors who would start businesses and boost the economy, and the reluctance of local officials to clamp down on foreign real estate investment, which can be a huge source of tax revenue for governments. "Canada has been saying for 20 or 30 years that we’re open for investment and immigration," Ley says. "But we’ve never developed the sophistication to move beyond that opening position."

Many politicians are understandably reluctant to get dragged into the dispute, lest they be seen as xenophobic or, worse, racist—so much so that Canada doesn’t even track how many foreigners own property in the country. B.C. Premier Christy Clark, for example, recently dismissed a petition with 18,000 signatures that called for a tax on foreigners who buy property in Vancouver by suggesting it would harm existing homeowners by causing prices to drop—which, of course, is precisely what those who signed the petition were hoping would happen. It’s also true that some developers have sought to play into Canadians’ hysteria about foreigners buying up all their houses. One B.C. condo marketer, for example, was disciplined last year for presenting two female employees—both Asian—as visiting Chinese condo buyers in front of local TV news cameras.

While Rabidoux is all for gathering more data on foreign purchasers of Canadian real estate, he doubts there are enough of them to make entire cities unaffordable. For that, Canadians have nobody to blame but themselves. "The story of unending foreign demand has probably propelled locals to make irrational purchases that are an even bigger driver in the market than the actual foreign investors," he says. He points to Toronto’s ballooning condo market, which is said to be rife with foreign speculators, as an example. The vast majority of the 50,000 or so units being built are increasingly tiny one-bedroom properties that can be priced in the sweet spot of a couple of hundred thousand each, he says. "Does that sound like some wealthy guy from China? Or is it more likely to be local investors who are price-sensitive, but are stretching to get into the market because they know everyone’s making money?" The industry would probably prefer that you didn’t bother to find out.

Back in Leaside, the neighbourhood continues to be ripped apart by construction-related disputes. Ellis, the lawyer, says he has helped at least three other local residents fight projects in their neighbourhood—most of which he believes are being coordinated by developers, as opposed to individual homebuyers. As for his own three-year war with his next-door neighbour, the battle seems to be finally drawing to a close. The property was purchased last year for just over $1 million by the son of another developer, who, despite initial plans to push forward with the existing project, has reluctantly agreed to tear down the structure—again—and start over. "Our argument was: ’Listen, this place has nothing to do with the overall look and feel of the neighbourhood, it’s a bad design and it’s ugly—just tear it down and rebuild,’" says Ellis, adding that the owner still stands to make a profit if he decides to flip it.

Think about that for a minute: You pay $1 million for a brand-new, almost-finished three-storey house, knock it down and build another house—almost equally large—and you still stand to make money in today’s real estate market.

And what happens if the current owner actually moves in? Says Ellis, "He’s going to have a pretty cold reception."

Related Posts

Inside an Ecohome on Stilts in Nova Scotia

Little House in the County

Inside a Salt-Sprayed Beach House in New Brunswick

The Great Unbuild

Get the Best of Maclean’s straight to your inbox.

Sign up for news, commentary and analysis. Join 60,000+ Canadian readers.