Attention boomers: Why demographics threatens your retirement

An entire generation might start selling soon…

Bird’s nest with empty eggshell

Share

One of the more worrying aspects of population aging is its effect on the prices of assets that many people are counting on to support them in retirement. For example, many Canadians may be planning to sell their house when they retire, buy a less-expensive condo and deposit the difference. The problem is that if a large wave of people retire and execute this strategy at the same time, the flood of new supply on the housing market will depress prices, thus reducing the value of the housing assets that were supposed to finance their retirements.

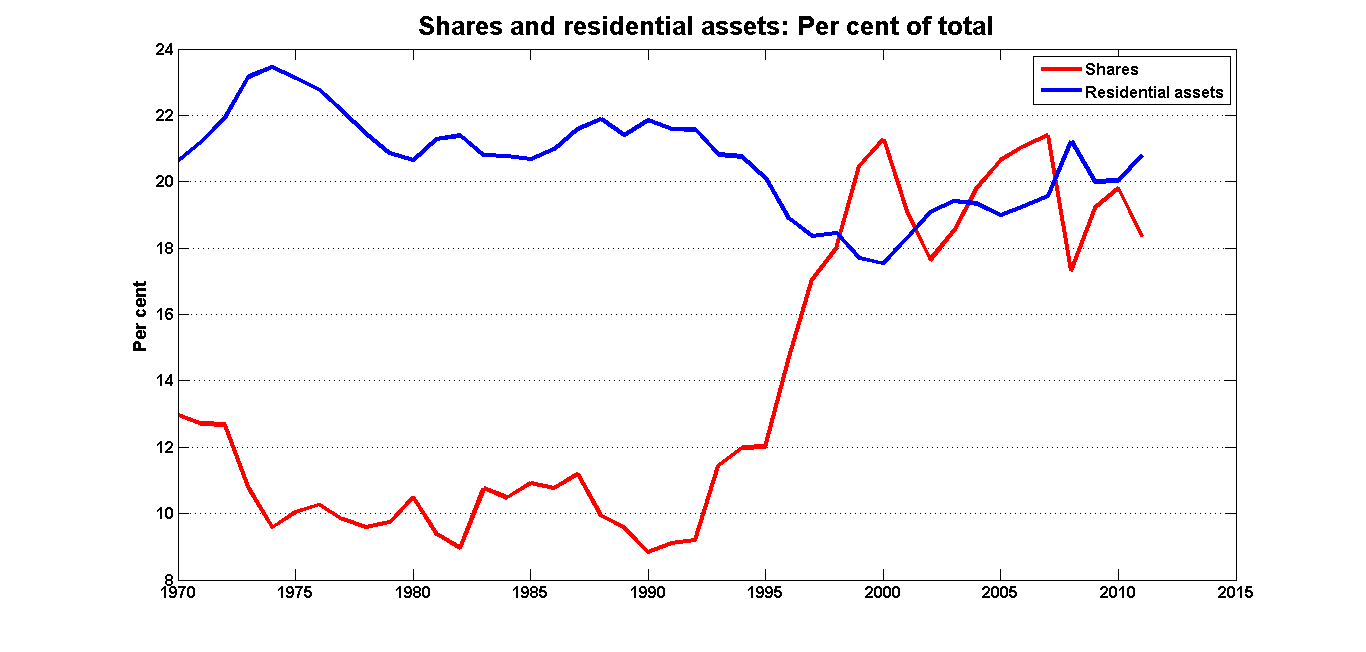

The run-up in housing prices over the past decade has attracted a lot of attention in this regard and led to worries that Canadian households’ balance sheets might be over-weighted on housing. But it turns out that much of the surge in the 2000s can be seen as a recovery from what was a very dismal market in the 1990s (see also this WCI post). Housing’s share of household assets did increase sharply during the 2000s, but this ratio still hasn’t recovered pre-1990 levels and remains below what it was in the 1970s. (Data are taken from Cansim Table 378-0051.)

The same holds for another type of asset: shares. Shares were 10 per cent of household assets for 20 years and doubled to 20 per cent during the mid-1990s, an increase that appears to be driven by higher stock prices, not by an increase in the number of shares held by households.

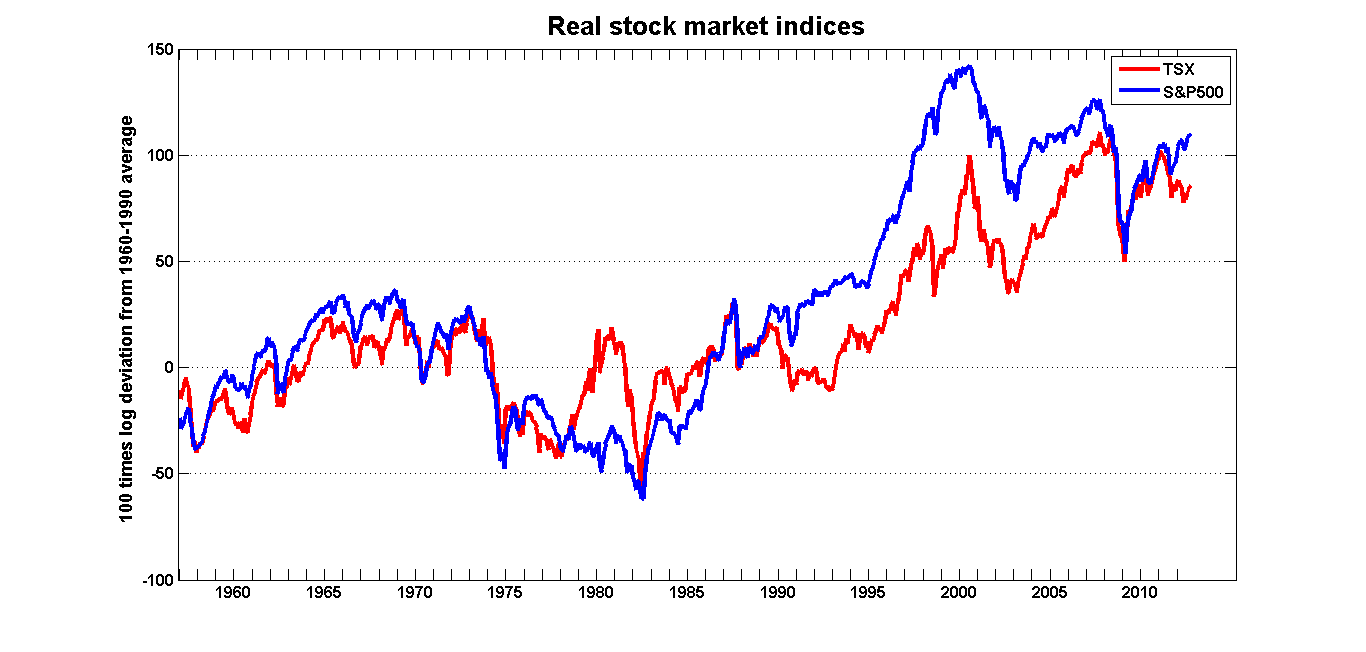

The next graph traces the evolution of the TSX and the S&P 500 stock indices, corrected for CPI inflation. The data are then scaled by their averages over 1960-1990, and are expressed in natural logarithms (logs). (The reason for taking the log transformation is that it makes the relative size of the changes more readily comparable across time: going from 10 to 20 generates the same movement in the graph as going from 100 to 200. For small changes, 100 times the difference in logs is approximately the same as a per cent change.)

In the 40 years before the mid-1990s, (real) stock prices fluctuated in what in retrospect looks like a fairly narrow band and without any discernible trend. But something happened twenty years ago that more than doubled share values in real terms. What?

There are many models and theories about the determinants of asset prices, but I can’t think of any whose fundamentals would explain increases of these magnitudes. There was the tech bubble during which fundamentals were abandoned, but the broader indices stayed high and continued to climb after the bubble popped.

The story that makes the most sense to me is demographics. In the mid-1990s, the baby boom cohort started entering its late thirties and forties—prime earning years—around this time, and they began to save for their retirements. This meant buying up assets, either directly (by means of individual plans such as RRSPs) or indirectly (by managers of pension plans). Demand outpaced supply, so prices increased.

But what will happen when the boomers start to retire? Will the process reverse itself, with a wave of selling forcing down prices and wiping out a generation’s retirement savings?