Seriously, no need to measure up to the U.S. on corporate tax rates

Uncle Sam is in a different league, writes Stephen Gordon

NDP leader Tom Mulcair speaks to the media on the steps of old city hall in Calgary, Thursday, July 12, 2012. Mulcair is visiting the city and taking in the Stampede which is celebrating its 100th anniversary featuring rodeo action, chuckwagon races, a midway, agricultural exhibits and live stock competitions. THE CANADIAN PRESS/Jeff McIntosh

Share

As Mike Moffatt has already noted, NDP leader Thomas Mulcair is responsible for what is probably the most ill-advised policy proposal of the year coming from a major federal party:

We will get back to something resembling the American combined rate in Canada which would indeed constitute an increase in corporate taxes.

Different taxes have different effects on economic growth, and the empirical consensus (example here; reading list here) is that corporate taxes are particularly harmful to it. Moreover, the increase in revenue they produce is small, so hiking up corporate taxes is a remarkably costly way of raising money.

You hear a lot about U.S. corporate tax rates from people who advocate increasing the Canadian rate — it’s implicitly suggested that there’s little harm in increasing Canadian corporate tax rates so long as they stay below U.S. rates. The problem is that there really isn’t any theoretical or empirical basis for thinking that this conjecture is plausible, much less solid enough to use as a fulcrum for policy.

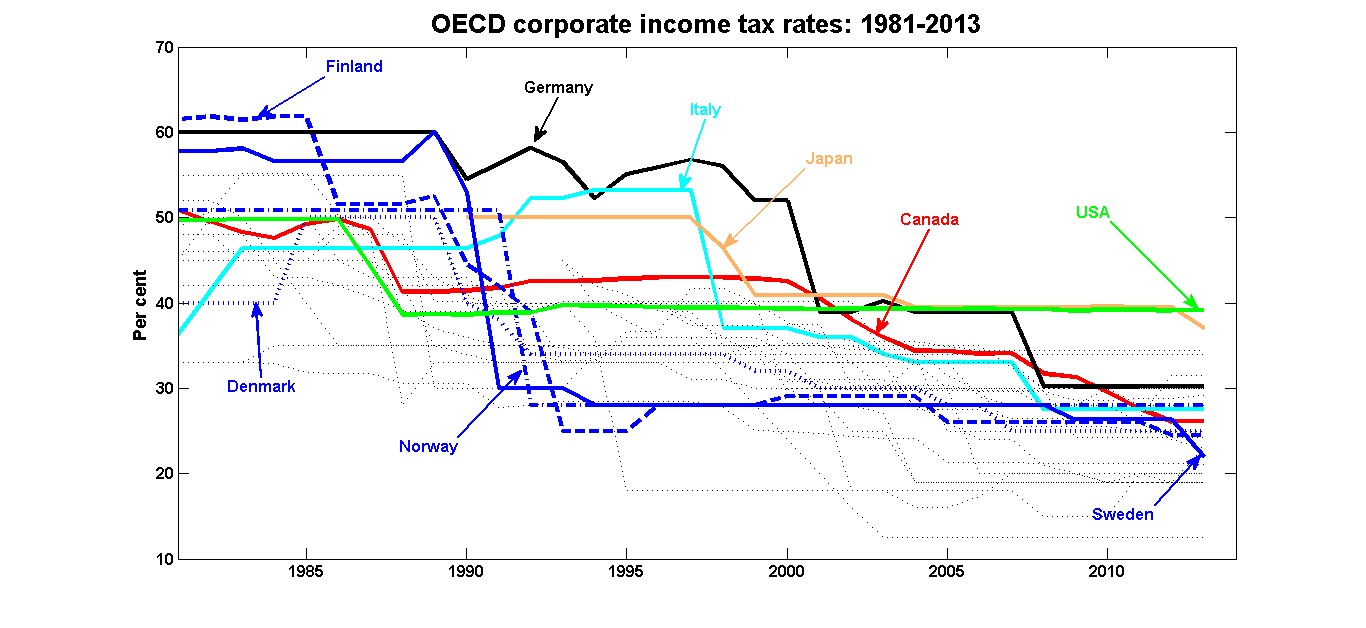

Firstly, a promise to keep rates below those of the U.S. should be put in context: U.S. corporate tax rates are the highest in the OECD. (Data source is Table II.1 from this page, click on the graph to open a larger version in a new window):

Promising to keep Canadian rates below those in the U.S. amounts to a promise to set them at the second-highest level in the OECD. Promising to keep them where they are, on the other hand, would place us comfortably among the Northern European welfare states.

Promising to keep Canadian rates below those in the U.S. amounts to a promise to set them at the second-highest level in the OECD. Promising to keep them where they are, on the other hand, would place us comfortably among the Northern European welfare states.

Also, I’m not aware of any theory of corporate tax rates in which an increase only bites once it crosses some threshold. An increase in corporate tax rates reduces the after-tax rate of return on all investment projects, and the problem is that projects that were viable at low rates will no longer be viable at higher rates. This doesn’t depend on what the level of U.S. tax rates is — although changes in U.S. rates can affect Canada (for example, some investors would react to an increase in U.S. rates by sending some of their savings up north).

But most importantly, the notion that Canadian policymakers can make the same choices as their U.S. counterparts when it comes to corporate tax policy is simply wrong: Even though the two economies are closely integrated, they operate in very different worlds when it comes to corporate income taxes.

The sheer size of the U.S. economy means that it plays a singular role in world markets. For one thing, even though the flows of goods and capital in and out out of the U.S. are huge, they are dwarfed by the size of its domestic markets. For many policy purposes, it’s not a bad assumption to assume that the U.S. economy is closed to trade. Arguments about the U.S. losing noticeable quantities of investment to other countries can ring hollow: Where, exactly, is all that capital supposed to go? It’s probably not a coincidence that the second-highest corporate tax rate is in the second-largest economy: Japan. Canada is a long way from playing in that league.

Moreover, the U.S.’ position at the centre of global financial markets means that many foreign investors see U.S. assets as very safe and are willing to hold such assets as a way of insuring themselves against risk and not necessarily as a way of generating returns. Even though the U.S. is a net debtor country (U.S. holdings of foreign assets are less than foreign holdings of U.S. assets), its investment balance is still positive: The rate of return on foreigners’ assets in the U.S. is significantly lower than the rate of return U.S. investors earn on foreign assets. The U.S. is the only country in the world that is able to pull off the trick of running a positive net international investment income balance on a negative net international investment position. If anything, the U.S.’ problem is that it currently attracts too much foreign investment. Again, this situation is far removed from the one facing Canada.

It is sometimes a good idea to refer to the U.S. as a benchmark, but not for corporate tax policy. The U.S. can indulge in practices we cannot afford.