I bet you didn’t know Canadian wages increased during the recession

We all know that employment falls during recessions, and many probably think it is equally evident that wages do as well. To be sure, there is downward pressure on wages, but sometimes the effect is barely perceptible.

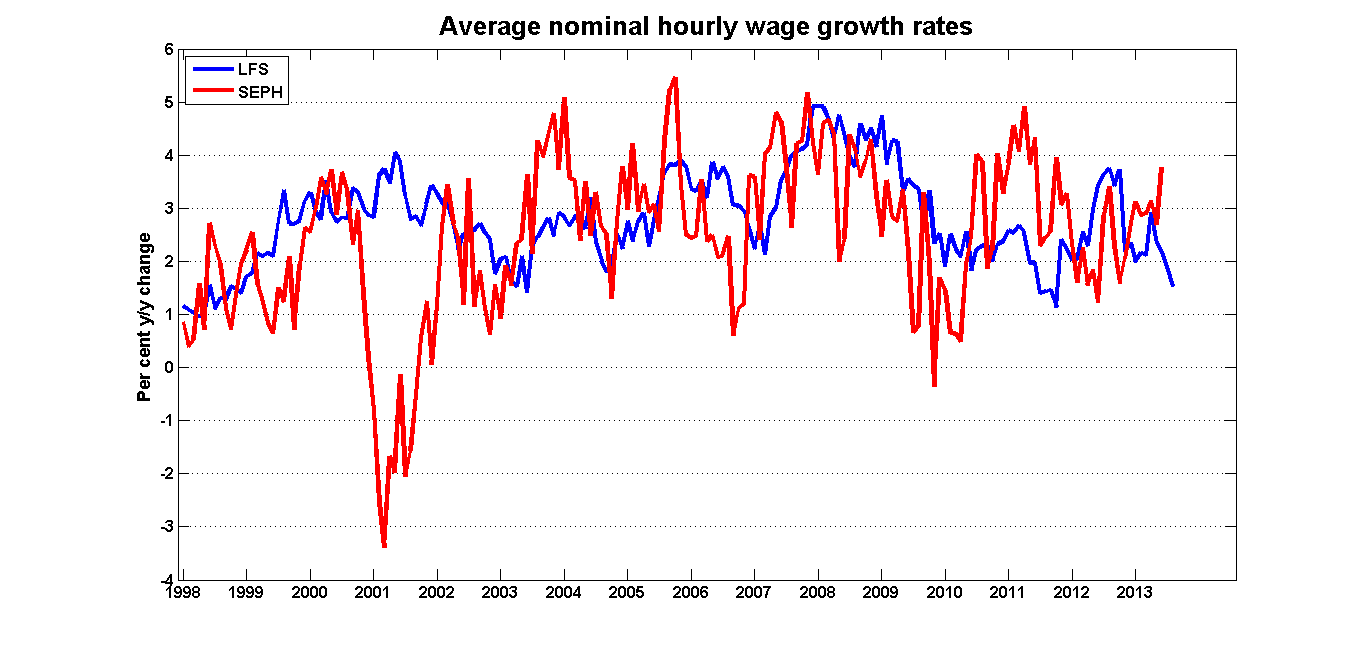

Here are the year-over-year growth rates of average hourly wages. The blue line is Labour Force Survey (LFS), and the red the Survey of Employment, Payroll and Hours data (SEPH). The two data sources use different methodologies — the LFS surveys households, and the SEPH surveys firms — and since there’s no obvious reason for using one and not the other, I’ll use both in this post.

Both series are quite volatile, but you can still see a reduction in wage growth in 2009. But wage growth picked up in subsequent years. If you smooth the not-seasonally-adjusted data by taking 12-month moving averages, it’s hard to detect a sustained reduction in nominal wages — or even in nominal wage growth — since the onset of recession:

This response — or rather, lack of a response — of wages to the decline in employment is one of the more enduring features and puzzles of macroeconomics. (In fact, it is arguably the reason why macroeconomics became a field of study in its own right.)

But changes in nominal wages (i.e. the dollar value of wages not adjusted for inflation) aren’t the same things as changes in workers’ buying power. Here are average hourly wages scaled by the Consumer Price Index (CPI), the most common measure of inflation, and expressed in constant 2012 dollars:

Related Posts

A once-bustling Greyhound rest stop sits empty. It’s a relic of a bygone era.

The Power List

The fact that workers’ purchasing power has increased during the recession will doubtlessly surprise many readers. But this increase in real wages is entirely understandable when you remember that one of the effects of the recession has been to drive CPI inflation below the Bank of Canada’s 2 per cent target. If you combine steady nominal wage growth with lower inflation, you get an increase in real wages. In order words, Canadians’ paycheques kept climbing but the price of the stuff they buy rose more slowly.

Still, that’s not the whole picture. The graph above is for hourly earnings — but one of the effects of the recession was to reduce hours worked. So here are average real weekly earnings:

It’s interesting that the slight dips in buying power occurred in 2011, after the jobs lost during the recession had been recovered.

Another consideration: So far, we’ve been talking about averages, which can be skewed by values at top or bottom end of the spectrum. What about the typical worker — or, statistically speaking, what about medians? The SEPH doesn’t sample workers, so it doesn’t provide data for median wages. The LFS does. Here are the real median hourly wages and weekly earnings:

The immediate effect of the recession was to sharply increase real wages, which goes a long way in explaining why employment growth has been so slow over the past few years. The quantity of labour demanded falls when real wages rise even — or perhaps especially — during recessions.

Monetary policy hasn’t quite worked as expected in the latest downturn. Normally, the Bank of Canada lowers interest rates during recessions in order to maintain its inflation target. This time, however, the Bank’s interventions were not enough to prevent inflation from drifting below two per cent during the past year or so.

If you were able to hold onto your job throughout the recession, you might well be in better financial shape now than you were four years ago: Not only has lower-than-expected inflation increased the purchasing power of your earnings, lower interest rates have also made it easier to service your debts.

The problem, of course, is that these charts are for wages, not incomes. There’s little consolation in knowing that wages have risen if you’re still unemployed.

Stephen Gordon is an economics professor at l’Université Laval in Quebec City. He started the blog Worthwhile Canadian Initiative in 2005 and has been blogging about economics ever since.

Related Posts

How these Québec-based businesses invested in energy efficiency

Who is Changpeng Zhao, Canada’s crypto king?

A Canadian company is changing the way we buy mattresses

Stephen Poloz on economic dangers ahead, staying positive and lessons from Star Trek

Get the Best of Maclean’s straight to your inbox.

Sign up for news, commentary and analysis. Join 60,000+ Canadian readers.