Coronavirus plunges Canada’s economy into the abyss

In every economic crisis over the last century, people have ultimately turned to the world of medicine to help make sense of the fear and uncertainty around them. In the 1930s, political cartoons showed U.S. president Franklin D. Roosevelt as a doctor tending to an ailing Uncle Sam, whose bandages carried words like “banking” and “depression.” When the 1990s currency crisis in southeast Asia threatened to infect the rest of the world and trigger a global meltdown, economists and investors took to calling it the “Asian flu.” And in 2008, as America’s economy was felled by the financial crisis, then president Barack Obama urged lawmakers to “provide a blood infusion” to “make sure that the patient is stabilized.”

Never has the metaphor of an economy on life support been more appropriate than for the twin health and economic crises the entire world now faces. Canada, like nearly every other nation on the planet, has put its economy into an induced coma as it attempts to fight off the invading COVID-19 virus. Offices, factories, stores and restaurants are closed and workers have been ordered to stay home, many without paycheques, some unsure whether their jobs will still exist when the crisis abates.

With each day bringing new tales of horror from overrun medical workers and stricter measures by governments to contain the virus, economists have scrambled to ratchet down their growth forecasts. At the Big Five banks, the average forecast among economists as of the end of March was for Canada’s economy to shrink by nearly 23 per cent in the second quarter on an annualized basis. (Less than two weeks earlier, they had predicted the decline would be half that bad.) Others forecast an even deeper drop—Capital Economics expects a contraction of 35 per cent.

READ: What to do if you’re laid off because of the coronavirus

An unprecedented one million Canadians applied for unemployment insurance in just one week in March. Officials are bracing for four million applicants when Ottawa’s newly created Canada Emergency Response Benefit launches on April 6.

We have moved with alarming speed past the question of whether Canada will endure a recession, and must instead now ask: How bad will it be, how long it will last and, perhaps most importantly, what comes afterwards?

Related Posts

Capitalism’s connection to our ever-worsening mental health

What Canada’s economic recovery might look like

“All we can say with any certainty right now is we’re facing a true economic abyss in the second quarter,” says economist David Rosenberg of Rosenberg Research in Toronto. “It’s going to look like the kind of economic decline we saw in the 1930s.”The good news, if that term can be used at all, lies in the aggressive steps taken by central banks and governments to tackle the downturn, which have reduced the likelihood of a credit crunch and financial crisis of the type we saw in 2008; or the 1930s, for that matter. “The Federal Reserve has done more in a month than they did in the first year of the Global Financial Crisis,” Rosenberg says. The same goes for the Bank of Canada, which slashed its overnight rate from 1.75 per cent to 0.25 per cent in the span of 23 days, while setting out to buy tens of billions worth of securities, like government bonds and corporate debt, in an effort to maintain liquidity in the market and keep credit flowing. The monetary ventilators are pumping full speed.

At the same time, the federal government has pledged massive sums of direct aid in the form of tax deferrals, loan guarantees and wage subsidies for small to mid-sized businesses. Taken together, Ottawa’s stimulation measures stood at more than $90 billion at the end of March, according to a Scotiabank economics report, or 4.5 per cent of GDP. Relative to the size of the economy, that’s three times more than Ottawa spent during the first year of the Great Recession.

Even that may not be enough. “My concern is that many of our programs have been put in place for a three-month period, but I am not convinced that the majority of those who are laid off will be rehired in three months,” says Frances Donald, chief economist with Manulife Investment Management. “It’s unlikely that all the damage that we withstand will be unwound at the speed it was initially drawn down.”

Yet while other countries, notably the U.S., are also grappling with these same uncertainties, Canada faces a set of circumstances that leaves the economy here particularly exposed. Before most Canadians had even heard of Wuhan or the emergence of a new coronavirus, Canada’s economy was flashing warning signs. Households were buckling under their debt loads, exports were weakening and businesses were retrenching—in the fourth quarter of 2019, the last before the novel coronavirus began to spread, Canada’s economy eked out growth of just 0.3 per cent. “Canada’s economy was running at stall speed even before this,” says Rosenberg, who adds the recent collapse in oil prices alone would have tipped Canada into a mini-recession.

That is going to put Canada’s eventual recovery even more at risk, and it raises a spectre that’s loomed over Canada’s economy for years—an end to the wealth-creation machine known as the Canadian housing market. “For a long time we’ve talked about what could pop a housing bubble,” says Donald. “You could pull back on the amount of people who want to buy a home, you could pull back on the amount of people who are able to buy a home, or you could see job losses.

“What we’re seeing now is that almost every element that could pop a housing bubble is now in place in Canada.”

Early in the crisis Larry Summers, who served as director of Obama’s National Economic Council, captured the surreal nature of this economic shock when he observed that “economic time has been stopped but financial time has not been stopped.” By that, he meant measures to slow COVID-19’s spread, like self-isolation and forced business closures, have stopped people from working and earning paycheques while decimating revenues for companies, but have not stopped the bills from piling up.

“The economy is a big beast and it will take at least six months to a year to get everything back onto some basic footing, whatever that normal will look like now,” says Scott Terrio, manager of consumer insolvency at Hoyes Michalos. “But for people’s personal budgets, financial time is still the same—everything is monthly or bi-weekly, or your truck payment is weekly. That doesn’t stop.”

The increasingly dramatic steps taken by Ottawa in March were aimed squarely at bringing the gears of the clock back into alignment. Prime Minister Justin Trudeau’s announcement that the government would boost its wage subsidy for small to medium-sized businesses from an initial paltry 10 per cent to 75 per cent, along with other financial assistance measures, will, it’s hoped, funnel enough money to Canadian workers who’ve been hit that they can provide for their families and stay on top of expenses. At the same time banks, with the government’s encouragement, have offered temporary mortgage deferrals of up to six months—according to the Canadian Bankers Association, nearly a quarter of a million Canadians have applied for relief—while Ottawa is leaning on credit card companies to cut their interest rates.

Time will tell if those measures are enough. The most optimistic view at this point is that self-isolation will bring the pandemic under control so that businesses can re-open and workers can begin to return to their jobs by this summer. “We believe the fiscal steps are enough to help propel the economy into a forceful recovery in the second half of the year,” Doug Porter, chief economist at BMO Capital Markets, stated in a report. In a March 27 forecast, BMO said growth would fall 25 per cent in the second quarter, followed by a 30 per cent jump in the third. Like a coiled spring, the theory goes, pent-up economic energy will quickly be released once the tension of the COVID-19 measures is eased.

But even if the economy reopens for business in relatively short order, there will still be a significant lag, says Stephen Brown, senior Canada economist at Capital Economics. He points to those parts of China where isolation orders have been lifted and people allowed to return to work. His firm’s daily activity gauge for China, which tracks things like freight traffic, property sales and electricity consumption, is running at 80 per cent of capacity. “People are still worried about going outside,” he says. “Everyone is well aware there could be another outbreak and you might have to repeat the whole process again.” If Canada’s economy rebounds sharply in the latter half of the year, Brown estimates GDP will still be 2.5 per cent below its pre-recession trend at the end of 2021.

What happens if self-isolation is required for a longer period? Canada’s deputy chief public health officer, Dr. Howard Njoo, has warned the country will be fighting COVID-19 for “months, many months.” Like that coiled spring, which loses its springiness if kept compressed too long, a prolonged shutdown of economic activity could result in structural weakness. Going into this crisis, Canada’s non-banking corporate sector had the third-highest debt-to-GDP level of all G20 nations behind only China and France, and the longer this goes on the greater the likelihood corporate bankruptcies will rise—as would the danger of a financial crisis that could seize up the country’s credit markets.

So a lot depends on how long these measures are in place. “It probably will be a V-shaped recovery if the shutdown is weeks or a month because people are very resilient,” says Livio Di Matteo, a professor of economics at Lakehead University. “If it stays shut down for six months—well, that’s a different ball game.”

It’s a scenario economists are struggling to model and understand. “The reopening of the economy will not depend on traditional economic drivers like demand and supply, but on the evolution of the health crisis,” says Donald. “As long as COVID-19 case counts are rising, this economy is not going to reopen and people will not be rehired. For the first time we are running economic analysis based off of health forecasts, of which we have very limited visibility and experience.”

Layered onto the COVID-19 crisis is the devastating impact of the collapse in oil prices. Amid plunging demand and a price war between OPEC and Russia, oil has fallen from US$63 a barrel for West Texas intermediate crude to less than US$20, the lowest level since 2002. At the same time, a barrel of Western Canada Select, the benchmark for Alberta oil sands crude, fell below US$5, down from US$63 at the start of the year. While the oil industry’s share of Canada’s economy had been somewhat reduced by the oil price rout in 2014, the energy sector still accounts for nine per cent of GDP and, with prices expected to remain low, oil will weigh down Canada’s post-coronavirus recovery.

There is also the sheer enormity of the job losses to consider. The list of companies announcing mass layoffs, even if temporary, is seemingly endless, and includes the airlines, Bombardier and automakers, not to mention restaurant, hotel, retail and theatre chains. Add to that the displaced army of workers employed by small and medium-sized businesses whose layoffs never make the news.

A report by the Canadian Centre for Policy Alternatives determined a “realistic case” could see the nation’s unemployment rate soar from 5.9 per cent in February to 13.5 per cent—the highest in 70 years.

Even if social distancing measures were to be lifted soon, some of those jobs are gone for good. Companies like Westjet and the Winnipeg bus manufacturer New Flyer Industries have said part of the cuts made in March will be permanent. Other businesses have closed shop entirely. Steve Nash Fitness World, a chain of 24 gyms across B.C., initially told its more than 1,000 employees they would be temporarily laid off. A week later, it sent out termination notices to all its staff.

At Hoyes Michalos, the insolvency firm where Terrio works, the vast majority of clients who come seeking debt relief during normal times are people who rent their homes, typically accounting for 93 per cent of filers. That’s dramatically shifted. Now half of those reaching out to the company are homeowners. It’s an extension of a trend Terrio began to see towards the end of last year, as the number of insolvency filings jumped 13 per cent annually, the fastest pace since the end of the Great Recession. “For many years Canadians have been binging on debt, and rising insolvency numbers were showing that was caving in on people,” says Terrio. “[COVID-19] has just poured kerosene on it and compressed everything that was going to happen over the next two years into a sudden crisis.”

Before the virus struck, there were signs of a housing rebound that might have helped indebted households put off dealing with financial problems. For two years, markets in several Canadian cities had slumped following rate hikes and tighter lending rules. But in February national home sales surged 27 per cent, sending prices up six per cent: the fastest pace since 2018. While western cities hit by slumping oil continued to struggle, in Toronto, Ottawa and Montreal, double digit gains and bidding wars were back and Vancouver saw annual price gains turn positive for the first time since 2018.

READ: Coronavirus in Canada: These charts show how our fight to ‘flatten the curve’ is going

Now the household debt overhang will make it harder for Canada’s economy to rebound. It’s one of the key differences between how the U.S. and Canada will fare in all this, says Manulife’s Donald. America’s housing crash last decade forced a reckoning that saw households reduce their leverage. As a result U.S. households “are fundamentally economically healthier and able to bounce back more quickly than Canadians,” she says. “The risk here is this pullback in economic activity takes much longer to rebound and creates offshoots of stress in the economy, not the least of which is the Canadian housing market.”

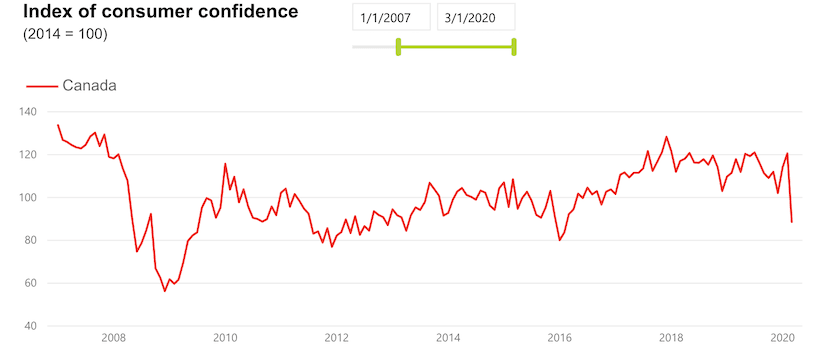

In announcing the Bank of Canada’s first of three 50-basis point cuts in March, Governor Stephen Poloz warned that declining consumer confidence “would naturally lead to reduced activity in the housing market . . . lower interest rates will actually help to stabilize the housing market, rather than contribute to froth.” The bank, along with the Canada Mortgage and Housing Corporation, is also buying up mortgages from lenders to inject cash into the financial system. The Bank of Canada pledged to buy up to $500 million a week of mortgages, while the taxpayer-funded agency CMHC committed to buy $150 billion of mortgages from banks, including previously uninsured, higher-risk mortgages. With three-quarters of Canada’s wealth tied up in real estate, and residential investment and household spending accounting for their largest share of GDP since at least the 1960s, it’s no surprise policy makers are desperate to forestall a real estate bust.

Yet economic forces seem destined to weigh down the market, not the least of which is instability in the job sector. “If we see a massive rise in unemployment, which is likely, those people are not going to be excited about buying homes and investors are not going to be excited about real estate as a way to make money when people can delay rent or mortgage payments,” says Donald.

The housing market also relied heavily on newcomers, and Rosenberg isn’t sure immigration will continue at the same pace. “It’s not going to zero, but we don’t know the extent to which it could be curtailed in an environment when globalization will come under pressure,” he says. “It’s very difficult to have a bullish view on Canadian housing, and that was the only positive story around.”

A housing correction would have a devastating effect on households who have already seen their investment portfolios decimated by the bear market in stocks. Roughly $1 trillion in wealth has been wiped out since February, with the S&P/TSX Composite Index plunging to the same level it was at in 2006. That will sap the ability of consumers to play the same saviour role that they did during the Great Recession, when the willingness of households to borrow and spend helped carry Canada through that crisis relatively unscathed. “Think of all the people who bought a condo in the last two years at sky-high prices with five per cent down,” says Terrio. “There’s going to be a lot of people going underwater, because they were so maxed out. They don’t have to sell their house just because it’s underwater, but it’s going to freak a lot of people out because their mindset was all about the free equity generated by rising prices.”

In the immediate term, Terrio believes insolvency filings will actually decline because of chaos in the banking and collections system and a backlog of civil cases. Once that clears, he expects insolvency numbers to spike to double what they were before the outbreak. In the meantime, he’s offering some advice. “If you bank with someone you owe money to, you need to change banks,” he says, pointing to a bank’s right to seize funds to cover debts, which could also put business and joint accounts at risk. “When times get tough people get desperate,” he says. “So do banks.”

One of the things that makes this moment so confounding is that we’re stranded between two economic worlds. Because of the standard delays in reporting statistics, upcoming economic data will relate to an old world that no longer exists. At the same time, we have no idea what the new world will look like. “As much as the next three months will be incredibly impactful, we need to monitor how many structural elements of our economy are about to change,” says Donald. “This is a short-term shock with extremely long-term repercussions.”

For one thing, the forces that drew the global economy closer over the past three decades are likely to reverse. Global supply chains have now suffered two massive shocks in short order, says Donald—tariffs and COVID-19. “Businesses are going to think twice about establishing global supply chains,” she says. Instead they’ll look closer to home, even if domestic suppliers are more costly, as insurance against future disruptions. It is likely that this could translate into higher costs for goods while also posing an export challenge for Canada.

Social distancing may also accelerate the work-from-home movement, as people adapt to technologies that let them work remotely, with ramifications for the commercial and residential real estate markets, says Donald. Likewise many people have been exposed to online shopping for the first time. “Our way of consuming things is going to change pretty radically even if this shock lasts only two to three months,” she says.

However things unfold, we’re likely to see western economies heavily dependent on government for the foreseeable future. “This might be the new normal,” says Rosenberg, “that to save capitalism, capitalism has to go on a long-term sabbatical. The government is taking over the economy by necessity.”

That means deficits the scale of which we haven’t seen in decades. An analysis by the Parliamentary Budget Office last month estimated the federal deficit for 2020-21 would amount to $113 billion, equal to 5.2 per cent of GDP, but that was before more recent emergency measures. Based on an estimate by the C.D. Howe Institute that a subsidy on that scale would work out to $82 billion over the three-month life of the program, the deficit next year could be closer to nine per cent of GDP. Scotiabank now estimates 10 per cent of GDP.

Ottawa insists Canada has a lot of fiscal room to deal with the crisis, and economists agree, noting that federal debt-to-GDP is the lowest in the G7. But while there is now a remarkable level of bi-partisan cooperation, and the costs are accepted as necessary, the fiscal fallout is certain to open up other issues in the long term that could add stress to the economy.

For now, though, the goal is to stabilize the patient. After all, as we’ve seen from this health crisis, those with pre-existing conditions—and Canada’s economy suffered from many—are often the most at risk.

This article appears in print in the May 2020 issue of Maclean’s magazine with the headline, “Into the economic abyss.” Subscribe to the monthly print magazine here.

MORE ABOUT CORONAVIRUS:

- Trudeau’s coronavirus update: ‘In the next 48 hours we will be receiving a shipment of millions of masks’ (Full transcript)

- In Doug Ford’s Ontario, knowledge is sorrow

- Inside the frantic, gruelling, all-hands-on-deck effort to bring Canadians home

- Coronavirus in Canada: These charts show how our fight to ‘flatten the curve’ is going

Jason Kirby is a Toronto-based editor and journalist. Follow him on Twitter: @jason_kirby

Related Posts

Mark Carney sits down with Paul Wells: Maclean’s in Conversation

What Canada can learn from Germany’s mass, unplanned migration

The ’safe bets’ and ’wild cards’ needed to meet Canada’s net zero emissions target

The working class has had enough

Get the Best of Maclean’s straight to your inbox.

Sign up for news, commentary and analysis. Join 60,000+ Canadian readers.